How Form 1099-DA Changes NFT Reporting

The 2026 tax season marks a structural shift in how digital assets are reported to the IRS. Under new final regulations, the responsibility for reporting sales and exchanges of digital assets moves from the taxpayer to the broker. This change is codified on the newly introduced Form 1099-DA, which replaces the fragmented self-reporting methods that have characterized the NFT market since its inception.

Brokers are now required to report transactions on or after January 1, 2025. For the upcoming filing season, most NFT sales will be pre-populated with cost basis data directly from the exchange or marketplace. The IRS will receive this data simultaneously, creating a system where discrepancies between what you report and what the broker reported are immediately visible.

Key takeaway: Broker reporting begins for transactions after Jan 1, 2025, with cost basis data required for 2026 filings.

For NFT owners, this ends the era of estimating gains from scattered wallet transactions. If you sold an AI-generated art piece or metaverse land parcel through a compliant platform in 2025, that platform must file a 1099-DA with the IRS and provide you with a copy. The form details the proceeds, cost basis, and holding period, simplifying the calculation of capital gains or losses.

However, this transition introduces complexity. Tax experts warn that the initial rollout will be "messy," as brokers reconcile historical data and adjust for varying platform definitions of "broker." If you traded NFTs across multiple platforms, you may receive several 1099-DA forms that need to be aggregated correctly on your return. The IRS has stated that additional guidance will be released to address these reconciliation issues, but the burden of accuracy now rests heavily on the intersection of your records and the broker’s filings.

The shift to broker reporting aims to close the compliance gap that has long plagued the digital asset space. By making the broker the primary reporting entity, the IRS expects to significantly increase voluntary compliance. For the average NFT holder, this means less manual tracking of individual sales, but it also means that every transaction is now on the record. Understanding the specific requirements of Form 1099-DA is no longer optional; it is the foundation of your tax strategy.

For the official text of the final regulations and related IRS guidance, see the IRS Newsroom page on broker reporting for digital assets.

Cost basis rules for AI art and metaverse land

The 2026 tax reporting changes introduce Form 1099-DA, shifting the burden of cost basis documentation from the investor to the broker. This transition is particularly complex for high-value digital assets like generative AI art and metaverse land. Unlike standard cryptocurrency trades, these assets often lack a centralized exchange history, making the accurate tracking of acquisition dates and original purchase prices difficult.

Under the new rules, brokers must report the cost basis for these digital assets alongside the gross proceeds. This requirement forces creators and collectors to maintain rigorous records of their initial minting costs or purchase prices. Failure to provide accurate cost basis data can result in the IRS treating the entire sale price as taxable gain, significantly increasing the tax liability for high-value transactions.

The distinction between standard crypto trades and these specific digital assets lies in their valuation and liquidity. Metaverse land and AI art are often illiquid and highly volatile, with prices that do not always reflect fair market value at the time of acquisition. This volatility complicates the determination of the initial cost basis, especially for assets acquired through secondary markets or decentralized platforms that do not provide detailed transaction histories.

| Feature | Standard Crypto Trades | AI Art & Metaverse Land |

|---|---|---|

| Broker Reporting | Mandatory cost basis reporting | Mandatory cost basis reporting |

| Cost Basis Tracking | Automated via exchange APIs | Often manual or fragmented |

| Valuation Stability | High liquidity, frequent pricing | Low liquidity, volatile pricing |

| IRS Treatment | Capital gains/losses | Capital gains/losses (complex basis) |

Investors holding these assets should anticipate more detailed reporting requirements. The new rules aim to close loopholes that allowed for underreporting of gains on digital assets. For AI art and metaverse land, this means that the initial purchase price must be clearly documented and reported. Without this documentation, taxpayers may face higher tax bills and potential penalties for inaccurate reporting.

Wallet-by-wallet accounting requirements

The IRS is shifting from a broad, aggregate view of crypto activity to a granular, transaction-level audit. For 2026 NFT tax reporting, aggregating data across wallets is no longer sufficient. The mandate requires you to track the cost basis and holding period for every individual wallet and exchange account separately.

This shift addresses the "mixing" problem. When you move assets between wallets or trade on decentralized exchanges, the IRS needs to see the exact origin of each token. If you combine data from five different wallets into one total gain, you lose the specific identification needed to calculate accurate capital gains. This is especially critical for AI art and metaverse land, where acquisition dates and initial minting costs can vary wildly.

To comply, you must export transaction histories from every source—MetaMask, Coinbase, OpenSea, and decentralized protocols. Reconcile these records to ensure no trade is double-counted or omitted. Experts warn that failure to provide wallet-specific data could trigger penalties or audits. Treat each wallet as a separate ledger, not just a different login credential.

Download CSV exports from all exchanges and wallet providers. Ensure the data includes timestamps, transaction hashes, and asset types. Do not rely on summary balances.

Calculate the original purchase price for each NFT or token within its specific wallet. This establishes your starting point for any future gain or loss.

Identify transfers between your own wallets. These are not taxable events, but they must be tracked to prevent double-counting when you eventually sell the asset.

Cross-reference your records with any 1099-DA forms received. Flag any discrepancies or missing transactions before filing.

-

Export CSVs from all wallets and exchanges

-

Reconcile basis for each individual wallet

-

Identify and flag unreported trades

Tracking basis across exchanges

The complexity increases when you consider that NFTs and digital assets often move through multiple venues. A piece of AI art might be minted on a decentralized platform, traded on OpenSea, and then held in a hardware wallet. Each step changes the context of the asset.

You must maintain a continuous chain of custody. If you sell an NFT on one exchange and buy another with the proceeds, the cost basis of the new asset is tied to the sale price of the old one. Failing to track this across platforms can lead to understated gains. The IRS views these as connected events, even if they happen on different servers.

For metaverse land, the stakes are higher due to the high value of these assets. A single parcel might appreciate significantly over years. Accurate record-keeping of the original purchase price, plus any improvements or transaction fees, is essential to avoid overpaying taxes on phantom gains.

| Source | Data Type | Relevance |

|---|---|---|

| Exchange 1099 | Summary | High for reporting, low for basis |

| Wallet CSV | Transaction-level | Critical for basis tracking |

| Smart Contract | On-chain | Verifies ownership and history |

The 2026 landscape demands precision. Aggregating data is a relic of the past; wallet-by-wallet accounting is the new standard. Prepare your records now to avoid the pitfalls of the upcoming filing season.

Choosing NFT Tax Software for 2026 Compliance

Selecting the right NFT tax software for 2026 compliance requires more than just basic transaction tracking. With the IRS implementing new broker reporting rules under Form 1099-DA, your software must accurately capture cost basis, holding periods, and specific metadata for complex assets like AI-generated art and metaverse land.

The primary challenge lies in handling the diverse data structures of NFTs. Unlike standard cryptocurrencies, NFTs often lack standardized identifiers, making it difficult for software to automatically categorize gains and losses. You need a tool that can parse on-chain data to generate accurate Form 8949 entries, ensuring that every sale, trade, or minting event is reported correctly.

When evaluating options, prioritize platforms that explicitly support the new 1099-DA data fields. Look for software that offers automated import from major exchanges and marketplaces, as manual entry increases the risk of errors. Additionally, verify that the software can handle AI art and metaverse land by checking if it supports custom metadata tagging or specific blockchain integrations relevant to these asset classes.

The following comparison highlights key features of leading NFT tax software providers to help you make an informed decision.

Common Mistakes in 2026 NFT Tax Filing

The 2026 filing season is shaping up to be a minefield for NFT investors, according to digital asset tax experts who warn that the new regulatory landscape will be messy and unforgiving. With the introduction of Form 1099-DA and stricter reporting requirements, even small oversights can trigger audits or unnecessary penalties.

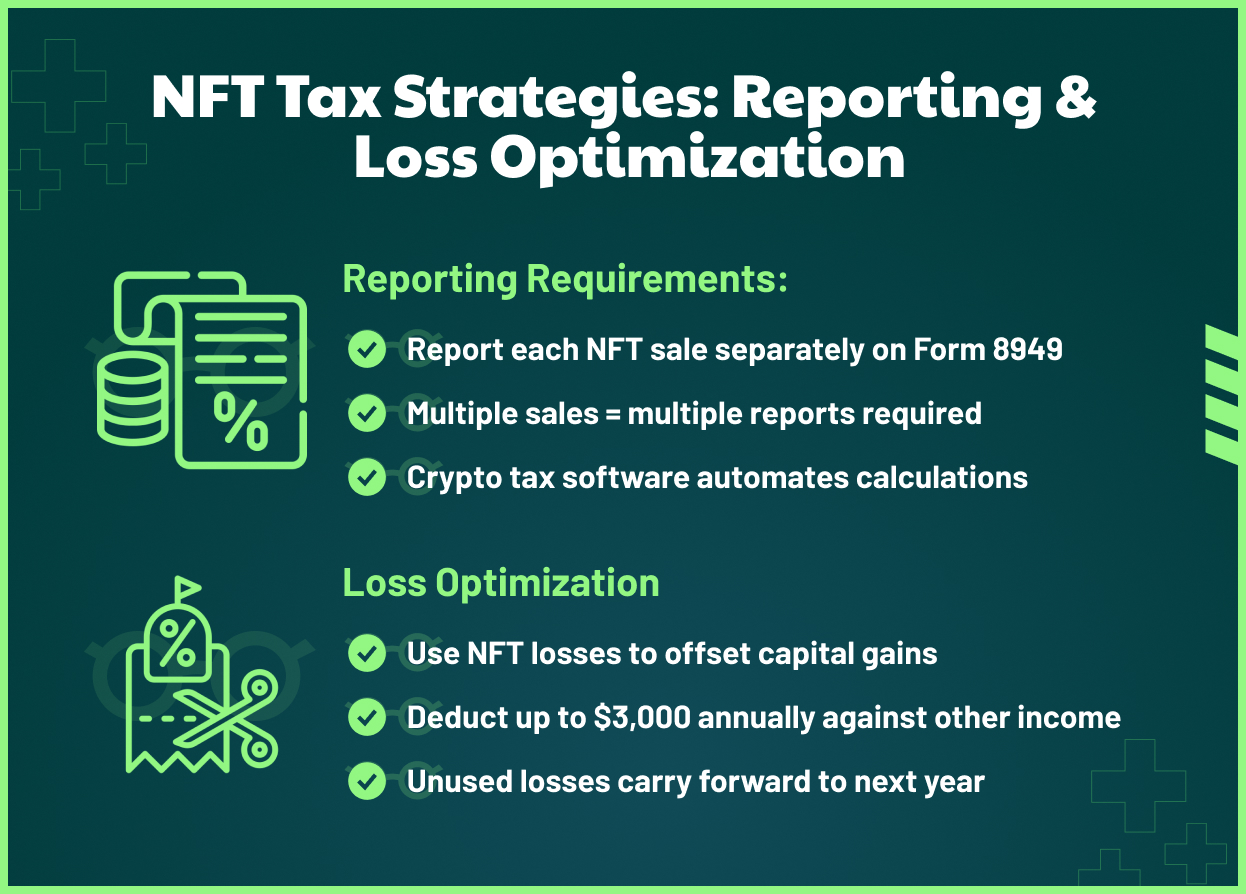

One of the most frequent errors is assuming that NFT transactions are immune to wash sale rules. While the IRS has not yet explicitly applied the traditional wash sale rule to NFTs, the distinction between "like-kind" exchanges has been eliminated for most crypto assets since 2018. Filing as if NFTs are exempt from these scrutiny mechanisms is a dangerous gamble. Investors must track every swap, trade, and marketplace transfer to prove the nature of the transaction if challenged.

Another critical pitfall involves AI-generated assets and airdrops. Many creators and collectors fail to report airdrops of AI-generated NFTs as taxable income at their fair market value on the date received. Whether the asset is a profile picture or a generative art piece, the IRS treats it as property. Ignoring these incoming assets means underreporting income, which can lead to back taxes and interest.

Finally, poor recordkeeping remains the biggest vulnerability. Without detailed logs of acquisition dates, costs, and disposal values, defending your position during an audit becomes nearly impossible. The new compliance environment demands precision, not approximation.

Frequently Asked Questions About NFT Taxes

The IRS treats digital assets as property. This means every transaction involving an NFT triggers a taxable event, regardless of whether the asset is a JPEG, a piece of generative AI art, or a virtual parcel in the metaverse. You must report gains and losses on your annual return, with rates determined by how long you held the asset.

Do you have to report NFTs on taxes?

Yes. No matter which category an NFT falls under, you'll need to report gains and losses on your annual tax return. Your tax rate is determined by how long you held the asset, along with your taxable income and filing status. In some cases, you might be able to deduct a capital loss to reduce your taxable income. Experian

When do new broker reporting rules take effect?

The IRS is phasing in stricter reporting requirements. While broker reporting begins in 2025, comprehensive cost basis and gain/loss data reporting for digital assets starts in 2026. This shift aims to close the information gap between exchanges and the IRS, making accurate record-keeping more critical than ever for NFT traders. Awaken Tax

How is AI-generated art taxed?

AI-generated art is taxed under the same property rules as traditional NFTs. The origin of the image does not change the tax treatment. If you mint and sell AI art, the profit is a capital gain. If you receive AI art as payment for services, it is ordinary income based on the fair market value at the time of receipt.

What about taxes on metaverse land?

Virtual land in the metaverse is treated as a capital asset. Buying, selling, or trading these parcels triggers capital gains tax. Unlike physical real estate, there are no exclusions for primary residences. Transactions involving metaverse land must be reported with the same precision as any other digital asset trade.

No comments yet. Be the first to share your thoughts!