DeFi Gas Fees Taxes 2026: FIFO LIFO HIFO Calculator for Ethereum Swaps Staking LP

With Ethereum trading at $2,318.54 amid a modest 24-hour gain of and $52.23, DeFi participants must grapple with the tax implications of every transaction, especially gas fees that now qualify as distinct taxable events under 2026 IRS rules. These fees, paid in ETH to process swaps, staking deposits, and liquidity provision, represent disposals that can generate capital gains or losses based on the fee’s fair market value versus its cost basis. For instance, spending 0.01 ETH valued at $2,318.54 with a $1,500 cost basis per ETH triggers a $81.85 gain per unit disposed. Ignoring this slices into your returns, particularly in high-volume DeFi strategies.

The shift to per-wallet cost basis tracking complicates matters further. Each wallet acts as its own silo, so FIFO, LIFO, or HIFO applies independently, preventing you from cherry-picking across addresses. This demands meticulous records, as tools tracking real-time cost basis become indispensable for DeFi transaction taxes 2026.

Gas Fees as Ethereum Taxable Events: The Mechanics

Every Ethereum transaction incurs gas fees, now explicitly treated as asset disposals per updated guidance. When you pay 0.02 ETH in gas for a swap, you’re selling that ETH at its spot price of $2,318.54, realizing gain or loss against your lot’s basis. Historical ambiguity has cleared: add fees to acquisition cost basis or subtract from sale proceeds only if not treated as separate disposals, but direct payments demand gain/loss computation.

Consider a liquidity pool addition: depositing ETH and a token pair costs gas equivalent to 0.015 ETH. At $2,318.54 per ETH, that’s $34.78 in value disposed. If your basis is lower, say $1,800, you owe tax on the $77.81 spread. Staking follows suit; claiming rewards might burn gas, layering another event atop ordinary income taxation of the rewards themselves.

Gas fees aren’t just operational costs; they’re miniature tax filings embedded in every block.

Mastering FIFO, LIFO, HIFO for Gas Fee Calculations

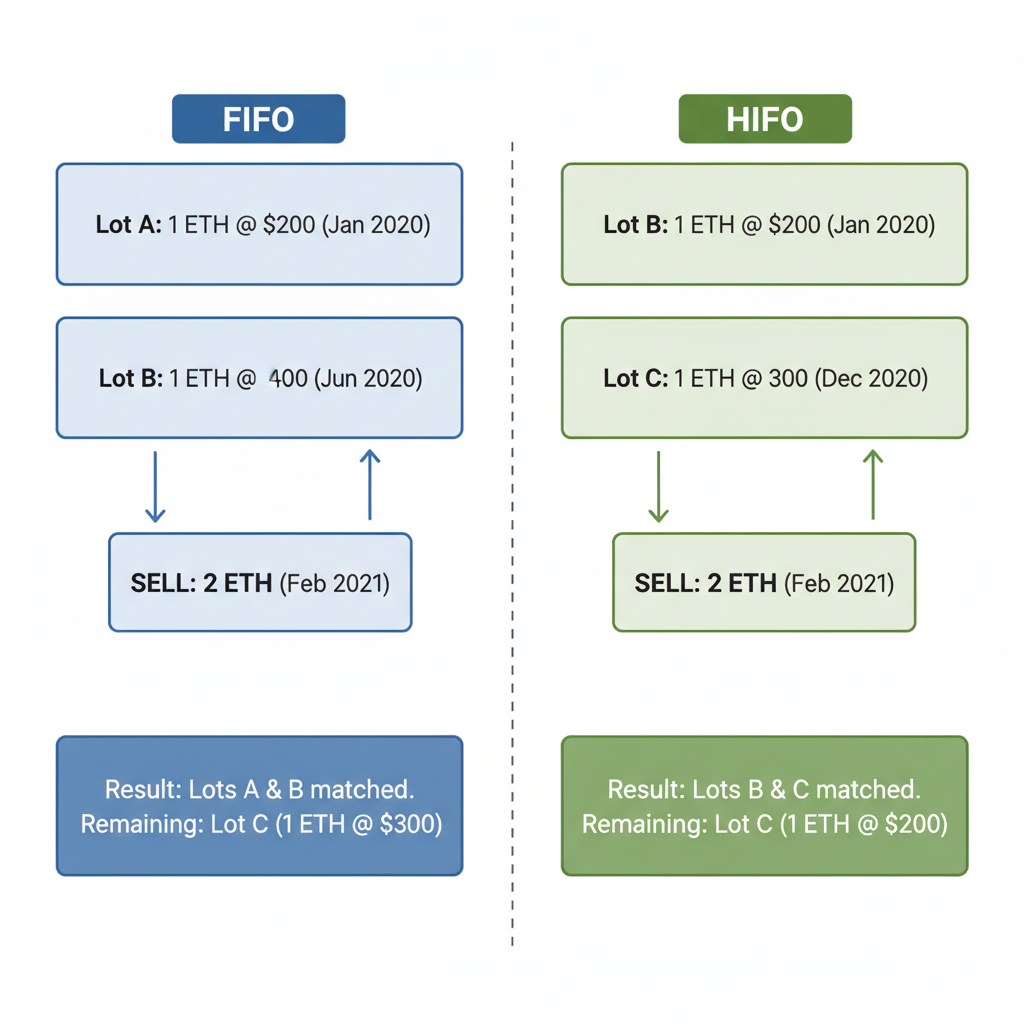

FIFO LIFO HIFO gas fees choices profoundly impact your tax bill, especially with Ethereum’s volatility. FIFO assumes first-in-first-out, suiting long-term holders but inflating gains in rising markets like today’s $2,318.54 level. LIFO reverses this, matching recent high-basis purchases first, potentially deferring taxes. HIFO, my preferred for optimization where documented, sells highest-cost lots first, minimizing realized gains most aggressively.

IRS permits Specific ID, FIFO, HIFO, and LIFO, but per-wallet silos mean strategy per address. For a trader with multiple ETH buys: $1,500 (Jan), $2,200 (Feb), $2,318.54 (Mar). Paying 0.01 ETH gas under HIFO uses the $2,200 lot, yielding minimal gain; FIFO hits the cheap Jan basis hard. Real-time calculators shine here, pulling historical prices to simulate outcomes.

Tax Lot Methods for 0.1 ETH Gas Fee at $2,318.54 FMV

| Method | Basis Used (per ETH) | Gain/Loss (for 0.1 ETH) |

|---|---|---|

| FIFO | $1,500 | $81.85 |

| LIFO | $2,318.54 | $0 |

| HIFO | $2,200 | $11.85 |

This table underscores HIFO’s edge for active DeFi users, though documentation is key to withstand audits.

Tax Treatment of Ethereum Swaps and Staking Rewards

Ethereum swaps exemplify ethereum gas taxable event layering. Swapping 1 ETH (basis $1,800) for USDC at $2,318.54 parity incurs gas of 0.01 ETH, plus the swap itself as a taxable exchange. Proceeds net gas value; calculate gain on both legs using your chosen method within the wallet.

Staking rewards hit as ordinary income at receipt fair market value, birthing new tax lots. A 0.05 ETH reward at $2,318.54 equals $115.93 income, basis set at that value. Subsequent gas to unstake or compound triggers capital events on those lots. Liquidity provision adds complexity: depositing into Uniswap LP tokens is an exchange, taxed on value differential, with gas amplifying it.

I’ve advised clients to model these via crypto gas fee calculator tools beforehand, avoiding year-end shocks. With Form 1099-DA looming, even non-broker DeFi stays reportable manually.

Ethereum (ETH) Price Prediction 2027-2032

Forecasts amid DeFi tax clarity on gas fees, staking, LP, and cost basis methods (FIFO/LIFO/HIFO), with EIP impacts and adoption trends

| Year | Minimum Price | Average Price | Maximum Price | YoY % Change (Avg from 2026) |

|---|---|---|---|---|

| 2027 | $2,800 | $4,000 | $6,500 | +43% |

| 2028 | $4,000 | $5,500 | $9,000 | +38% |

| 2029 | $5,000 | $7,200 | $11,500 | +31% |

| 2030 | $6,500 | $9,500 | $15,000 | +32% |

| 2031 | $8,000 | $12,000 | $19,000 | +26% |

| 2032 | $10,000 | $15,500 | $24,000 | +29% |

Price Prediction Summary

Ethereum’s price is projected to grow progressively from 2027-2032, fueled by DeFi adoption post-2026 tax regulations, gas fee optimizations via EIPs, and staking/LP incentives. Average prices rise from $4,000 to $15,500, with min/max reflecting bearish corrections and bullish surges, assuming market cycles and regulatory tailwinds.

Key Factors Affecting Ethereum Price

- DeFi tax clarity (gas fees as cost basis adjustments, FIFO/LIFO/HIFO tracking per wallet) boosting user participation

- EIP upgrades reducing fees and enhancing scalability for swaps/staking/LP

- Staking rewards taxed on receipt, increasing ETH demand as income asset

- Regulatory developments like 1099-DA and per-wallet silos reducing compliance friction

- Market cycles: recovery post-2026, institutional adoption amid competition from L2s

- Overall crypto market cap expansion and Ethereum’s dominance in DeFi TVL

Disclaimer: Cryptocurrency price predictions are speculative and based on current market analysis.

Actual prices may vary significantly due to market volatility, regulatory changes, and other factors.

Always do your own research before making investment decisions.

Non-broker DeFi events like these demand self-tracking, as 1099-DA focuses on centralized platforms. Liquidity providers face dual hits: the LP deposit as a swap-like exchange and gas as a disposal. Withdrawals reverse it, taxing impermanent loss alongside fees. I’ve seen portfolios swing 20% post-tax due to overlooked layers.

Liquidity Provision Deep Dive: Tax Layers Exposed

Adding ETH-USDC to a pool yields LP tokens valued near deposit fair market value, but any spread triggers gain. Gas at 0.015 ETH amid $2,318.54 pricing disposes that slice first. Under LIFO, recent buys cushion it; FIFO exposes early lows. Rewards from fees accrue as income, compounding tax lots. Unstaking LPs reverses the exchange, with gas again intervening. Per-wallet rules isolate strategies: a hot trading wallet on HIFO thrives, while a cold HODL on FIFO lags.

LP isn’t passive income; it’s a tax pinata, bursting with reportable events at every interaction.

For defi transaction taxes 2026, aggregate these meticulously. A single pool cycle might spawn four events: deposit exchange, deposit gas, withdrawal exchange, withdrawal gas. Staking atop LPs? Layer income on top. Ethereum’s base layer speed-ups via L2s cut fees but don’t erase tax math; they just shrink the ETH disposed.

Calculate DeFi Swap Taxes: FIFO/HIFO with Gas Fees (ETH $2,318.54 FMV)

This process, repeated per transaction, explains why manual spreadsheets crumble under DeFi volume. Real-time platforms auto-apply fifo lifo hifo gas fees, fetching $2,318.54 spots and historicals for precision.

Per-Wallet Silos: Strategy Shift Required

IRS’s wallet-centric tracking upends cross-address optimization. Your MetaMask at HIFO can’t offset Ledger’s FIFO losses; each stands alone. Migrate wisely or segment intents: aggressive DeFi in one, staking in another. For gas-heavy swaps, pre-position high-basis ETH in active wallets. At $2,318.54, buying dips builds buffers for upcoming fees.

Staking nuances persist: Revenue Ruling 2014-21 locks rewards as income at receipt, basis equals that value. Gas to claim? Separate disposal. I’ve optimized client farms by batching claims, minimizing fee events while HIFO chews expensive lots.

Form 1099-DA eases CEX reporting but spotlights DeFi gaps. Brokers issue for swaps; you handle Uniswap manually. Safe harbors for 2025 transitions fade by 2026, demanding basis substantiation. Audit-proof with API-connected calculators exporting CSV for TurboTax or pros.

Tools and Optimization: Stay Compliant, Maximize HODL

As a CPA steering DeFi portfolios, I champion HIFO where records permit; it surgically trims gains without FIFO’s bull-market bite. Pair with crypto gas fee calculator simulating 2026 scenarios at $2,318.54 ETH. Test LIFO for short-term flips, FIFO for buy-and-forget. Per-wallet dashboards reveal silos’ interplay, forecasting bills pre-filing.

Gas optimization ties in: batch transactions during low network congestion, use EIP-1559 tips sparingly. L2s like Optimism slash ETH outlay, deferring disposals. Deduct unreimbursed fees? Only as miscellany if itemizing, post-TCJA caps. Track everything; volatility at $2,318.54 turns 0.01 ETH fees into $23 swings.

DeFi’s tax maze rewards the prepared. Model gas as disposals, silo per wallet, method-match ruthlessly. Platforms like ours at NFT Tax Pro crunch FIFO/LIFO/HIFO for swaps, staking, LPs in real-time, spitting IRS-ready forms. Your edge lies in foresight: compute today, compound tomorrow.