DeFi traders in the UK have long navigated a tax minefield when providing liquidity or lending assets, often facing immediate capital gains tax (CGT) hits on transactions that barely moved the economic needle. Enter the proposed UK DeFi no gain no loss tax rule for 2026, a game-changer from HM Revenue and Customs (HMRC) that promises to treat many liquidity pool deposits and lending activities as no gain, no loss (NGNL). This deferral mechanism sidesteps premature CGT triggers, letting you hold positions without tax drag until a genuine disposal crystallizes profits or losses. As markets evolve and volumes swell, this aligns UK rules with DeFi's reality, potentially unlocking billions in trapped capital for reinvestment.

HMRC's consultation outcomes, detailed in their November 2025 summary, confirm broad industry backing from players like Aave, Binance, and Deloitte. The core idea: if you deposit tokens into a pool or lending protocol and withdraw equivalent value later, no CGT event occurs at entry or interim steps. Tax bites only on true economic disposals, such as selling for fiat or receiving mismatched tokens reflecting impermanent loss. This tackles the absurdity of taxing volatility-driven pool adjustments as disposals, a stance I've critiqued for years in macro crypto tax analysis.

Decoding NGNL: DeFi's Tax Lifeline Against Over-Taxation

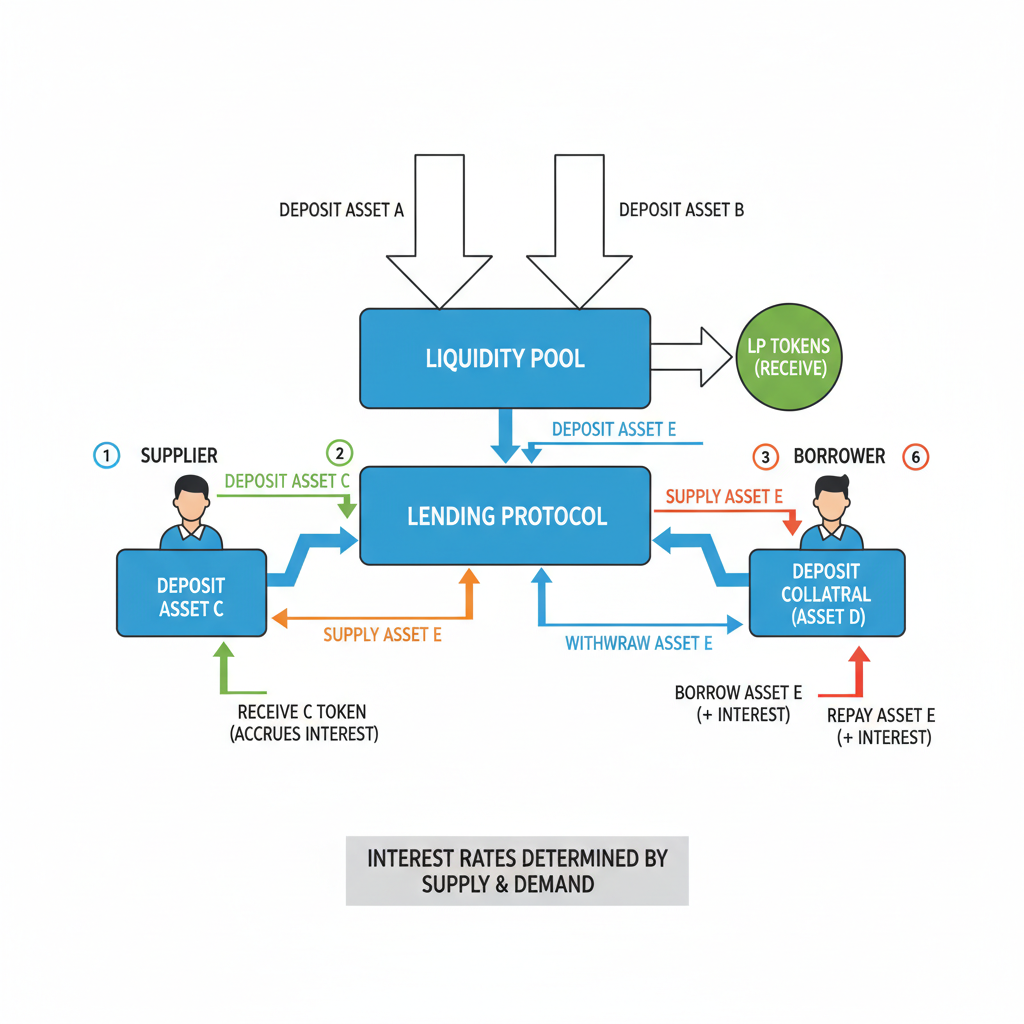

The NGNL treatment draws from established CGT reliefs, like no gain no loss transfers between spouses, but tailored for decentralised protocols. Under current rules, staking or lending often counts as a disposal, forcing cost basis recalculations mid-position - a compliance nightmare amid thousands of micro-transactions. HMRC's fix: defer recognition until exit, preserving your original acquisition cost for final computation.

Consider a single-token loan on Aave: deposit ETH at £2,500 cost basis, borrow against it, accrue interest. Pre-2026, lending might trigger CGT on any value fluctuation. Post-reform, NGNL holds the fort; tax applies solely if withdrawal yields more or less ETH than deposited, benchmarked against pool economics. Multi-token automated market makers (AMMs) like Uniswap get similar grace, taxing deviations from contributed ratios rather than every rebalance.

HMRC's approach ensures taxation mirrors economic substance, not protocol mechanics - a principled pivot long overdue.

Yet caveats loom: tokenized real-world assets or security-like tokens may fall outside, demanding careful classification. High-volume users face reporting burdens, as HMRC eyes transaction logs for audits. My view? This NGNL framework fortifies long-term DeFi yields, but demands meticulous records to prove 'no economic change' on exit.

Liquidity Pools Under the Microscope: Rethinking UK Liquidity Pool Taxes 2026

UK liquidity pool taxes 2026 shift dramatically with NGNL. Picture adding equal-value ETH-USDC to a Curve pool. Impermanent loss erodes value over time, but pre-reform, deposit and reward claims could each spark CGT. Now, entry is NGNL; ongoing fees or swaps within the pool defer tax. Crystallization hits on withdrawal: if you get back 1.05 ETH and 1.05 USDC equivalents, gain on that 5% uplift. Fewer tokens? Loss offsets future gains.

This UK crypto DeFi tax deferral eases cash flow for LPs, vital in volatile markets where early tax eroded yields. Deloitte's TaxScape notes it covers most staking/lending DeFi setups, excluding yield-bearing synthetics potentially deemed income. Opinion: Providers win big, as reduced friction boosts TVL; retail users gain simplicity, but pros must model impermanent loss precisely for accurate basis tracking.

Real-world math underscores the relief. Deposit £10,000 pool position at t=0. ETH surges 50%, USDC stable - pool rebalances, your share now £12,000 market value but locked basis. Pre-NGNL, harvest might tax phantom gains; NGNL waits for unwind, taxing only net outcome. Essential for defi pool deposit taxable uk clarity.

DeFi Lending: Capital Gains Relief That Lenders Deserve

DeFi lending capital gains UK woes end with NGNL extending to protocols like Compound or Euler. Lend BTC, earn COMP rewards - was lending a disposal? Exit with principal plus interest? Under proposals, NGNL blankets entry and steady-state; tax on rewards as miscellaneous income (0-45%), principal mismatches as CGT (18-24%). HMRC specifies conditions: same-token returns without economic alteration qualify.

GOV. UK consultations highlight crypto borrowing too - collateral stays yours, no disposal until liquidation. This prevents double-taxation traps, where borrow-repay cycles multiplied events. From my 18-year macro lens, it's a regulatory nod to DeFi's maturation, mirroring traditional finance's substance-over-form tests.

Stakeholders cheer, but fine-tuning persists: volume thresholds? On-chain proof mandates? As February 2026 updates affirm ongoing dialogue, expect legislation soon, possibly Autumn Budget tweaks.

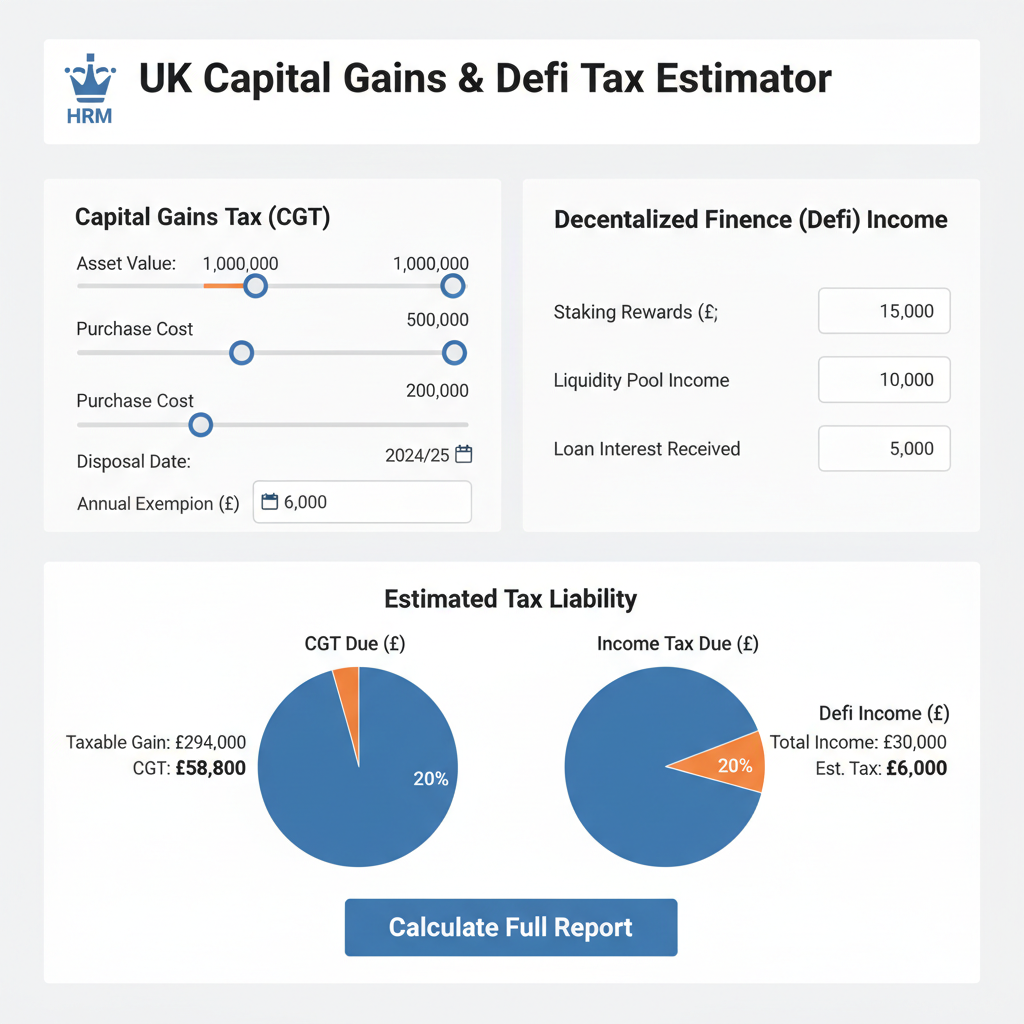

Implementing NGNL demands precision in tracking entries and exits, where tools like real-time tax calculators become indispensable. High-frequency DeFi users generate transaction volumes that manual spreadsheets can't handle, risking audit flags from HMRC's data-matching with exchanges. Platforms optimized for FIFO, LIFO, and HIFO methods, attuned to NGNL deferrals, project net tax liabilities upfront, factoring impermanent loss and reward accruals.

Tax Scenarios Unpacked: NGNL in Action for Pools and Lending

To grasp UK DeFi no gain no loss tax impacts, dissect common setups. Single-sided staking: deposit 1 ETH at £2,000 acquisition cost, withdraw 1 ETH plus 0.05 ETH rewards after six months. NGNL ignores entry; principal return is neutral, rewards taxed as income at your marginal rate. Multi-asset pools introduce nuance: contribute 1 ETH (£2,500) and £2,500 USDC, exit with 0.95 ETH (£3,000 market) and £2,800 USDC due to arbitrage. Gain computation uses original pooled basis, taxing the net uplift or loss.

UK DeFi NGNL Tax Scenarios: Pre- vs Post-2026

| Activity | Pre-2026 Tax Event | Post-NGNL Treatment (2026+) | Example Gain/Loss |

|---|---|---|---|

| Liquidity Pool Deposit | Taxable disposal (CGT on unrealised gains) | No gain/no loss relief (tax deferred until economic disposal) | Deposit appreciated tokens 📈: No CGT triggered ✅ |

| Liquidity Pool Withdrawal (same tokens) | Taxable disposal of LP position (CGT) | No gain/no loss if identical quantity returned | Withdraw same amount ⚖️: No tax on interim moves ✅ |

| Liquidity Pool Withdrawal (altered tokens) | Taxable disposal (CGT on gain/loss) | Tax only on actual economic gain/loss | More tokens returned 💰: CGT on difference / Fewer 📉: Relief on loss |

| DeFi Lending Entry | Taxable disposal (CGT event) | No gain/no loss (base cost preserved) | Lend appreciated tokens 📈: Tax deferred ✅ |

| DeFi Lending Exit (same tokens) | Taxable repayment/receipt (CGT) | No gain/no loss if same returned | Retrieve principal ⚖️: No CGT on return ✅ |

| DeFi Lending Exit (with rewards) | Taxable (CGT + income tax on rewards) | CGT on principal change + income tax on rewards | Principal same ⚖️ + rewards 💹: Income tax only on rewards |

These examples spotlight why deferral matters: it prevents over-taxation on paper gains that vanish with market swings. From a conservative standpoint, NGNL encourages patient capital allocation, curbing short-term speculation that plagues retail DeFi participation. Yet, it underscores record-keeping imperatives; on-chain proofs via Etherscan or protocol dashboards must align with Self Assessment filings.

Mastering Compliance: Step-by-Step NGNL Tax Calculation Guide

Navigating defi lending capital gains UK post-reform requires systematic workflows. Start by segregating NGNL-qualifying activities from taxable ones, like outright swaps or airdrop claims. Real-time calculators automate this, ingesting wallet data to flag deferrals and compute crystallized events.

Master UK DeFi NGNL Tax Calculations: 2026 Liquidity & Lending Guide

This process, when powered by advanced platforms, handles complexities like flash loans or layered positions across chains. My macro research reveals regulatory shifts like NGNL stabilize yields; expect 10-20% TVL uplift in compliant protocols as tax certainty draws institutions. But beware exclusions: if pools involve security tokens or RWAs, traditional CGT applies from inception, per HMRC's substance tests.

For lending, differentiate principal from yields. Protocols distributing governance tokens? Those often hit as income immediately, outside NGNL. Borrowing against collateral? NGNL shields until liquidation, preserving basis through repay cycles. High-volume traders, tally transactions exceeding HMRC thresholds - proposals hint at 1,000 and events triggering enhanced scrutiny.

NGNL isn't a free pass; it's a deferral demanding ironclad provenance to withstand audits.

Income tax layers add depth: staking rewards or pool fees, post-NGNL, face 0-45% rates, potentially deductible against trading losses. Contrast with CGT's 18-24% band; strategic structuring - pools for growth, lending for income - optimizes brackets. In volatile regimes, this flexibility proves golden.

Tools of the Trade: Real-Time Calculators for 2026 DeFi Taxes

As UK liquidity pool taxes 2026 evolve, manual compliance crumbles under DeFi's scale. Enter specialized calculators like NFT Tax Pro, engineered for NGNL workflows. They ingest API feeds from Uniswap, Aave, ingesting cost basis in real-time, simulating exits to forecast liabilities. Features span multi-method accounting, impermanent loss modeling, and HMRC-ready reports - vital for UK crypto DeFi tax deferral adherents.

Why prioritize such tools? Audits loom larger with 2026's international data-sharing pacts, per BDO insights. Calculators auto-generate audit trails, apportioning basis across forked tokens or migrated pools. For pros, HIFO selection maximizes deferrals; novices appreciate drag-and-drop wallet syncs. In my view, this tech bridges DeFi's innovation with UK's conservative tax ethos, fostering sustainable growth.

Stakeholder consultations continue, refining edges like cross-chain applicability or oracle dependencies. Until legislation lands, adopt NGNL conservatively, consulting advisors for edge cases. This regime positions UK DeFi as a compliant haven, rewarding fundamentals over frenzy.

No comments yet. Be the first to share your thoughts!