In the volatile world of DeFi, providing liquidity to pools on platforms like Uniswap can supercharge your yields, but 2026 IRS rules turn those rewards into a tax minefield. With mandatory FIFO reporting kicking in January 1, DeFi liquidity taxes demand sharp strategies to protect your gains. Imagine depositing tokens into a liquidity pool only to face unexpected capital gains taxes upon withdrawal; that's the reality reshaping defi yield farming taxes 2026. As a CFA with deep roots in portfolio management, I advocate flipping the script: master FIFO versus HIFO to not just comply, but thrive.

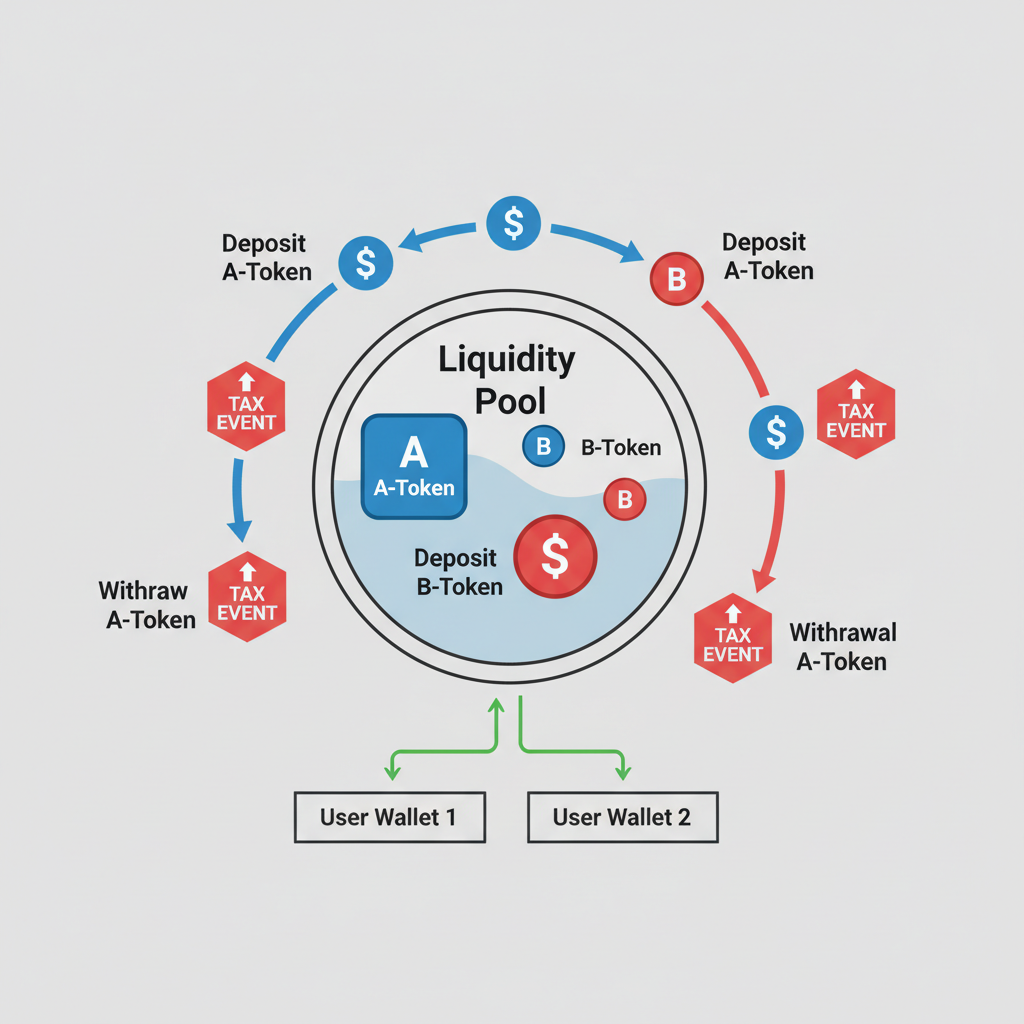

DeFi liquidity provision thrives on pairing assets like ETH-USDC to earn fees, yet each deposit triggers a taxable disposition. Withdrawals compound the complexity, calculating gains from deposit value to exit value, including accrued LP tokens. Impermanent loss adds another layer, potentially crystallizing losses you must harvest strategically. This isn't mere bookkeeping; it's about architecting your tax posture amid wallet-by-wallet tracking mandates.

Decoding 2026 IRS Mandates: FIFO Takes Center Stage

The IRS's pivot to mandatory FIFO for broker-reported crypto transactions starting 2026 levels the playing field, but unevenly. Brokers must default to First In, First Out, assuming your oldest assets sell first. In bull markets, this spells trouble for fifo defi cost basis: low-cost basis from early buys inflates taxable gains on liquidity exits. Picture buying ETH at $1,000, adding to a pool years later when it's $4,000, then withdrawing amid a surge; FIFO tags massive short-term gains, hiking your bracket.

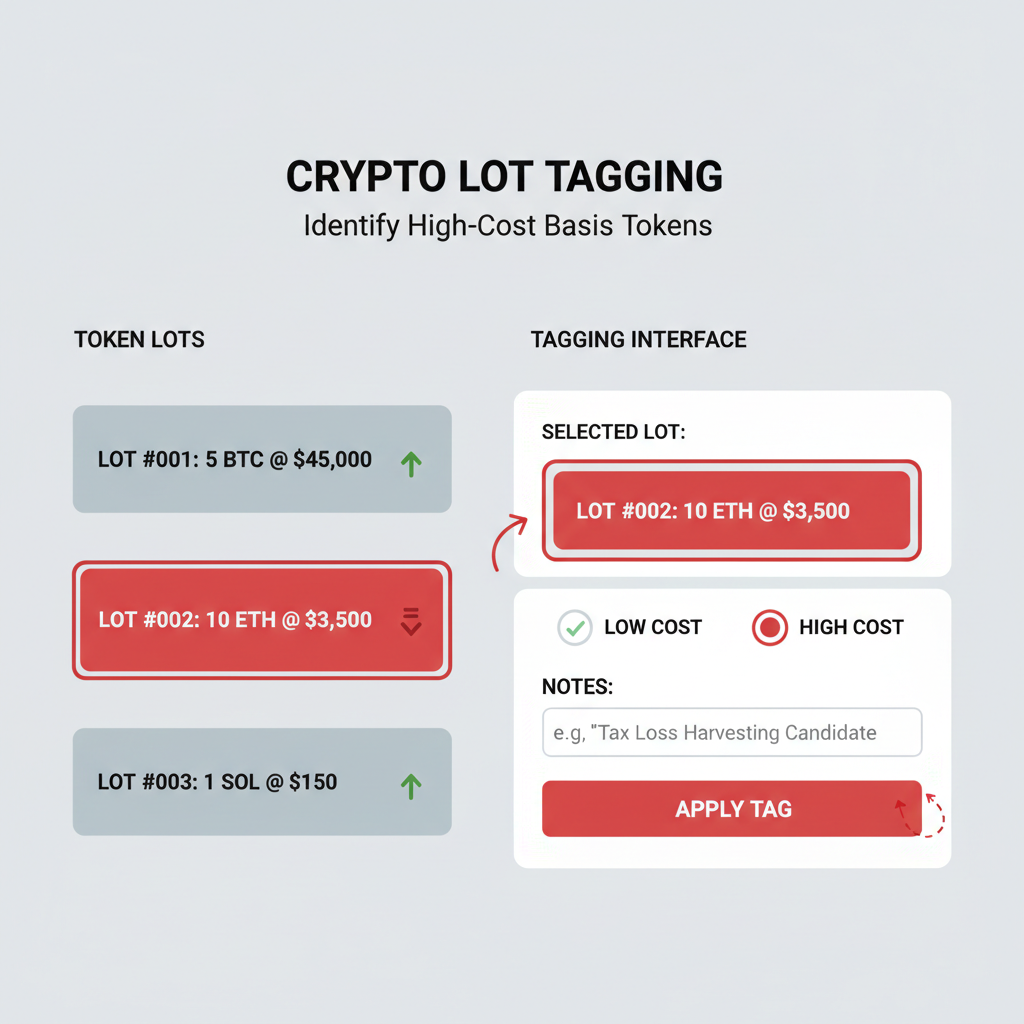

Yet, empowerment lies in exceptions. Specific Identification lets you cherry-pick units via HIFO, selling highest-cost first to slash gains. But it demands real-time records: lot, date, cost basis, fair market value at sale. No retrofits; miss the window, and FIFO locks in. Wallet-by-wallet silos amplify this: treat each DeFi wallet separately, tracking deposits meticulously.

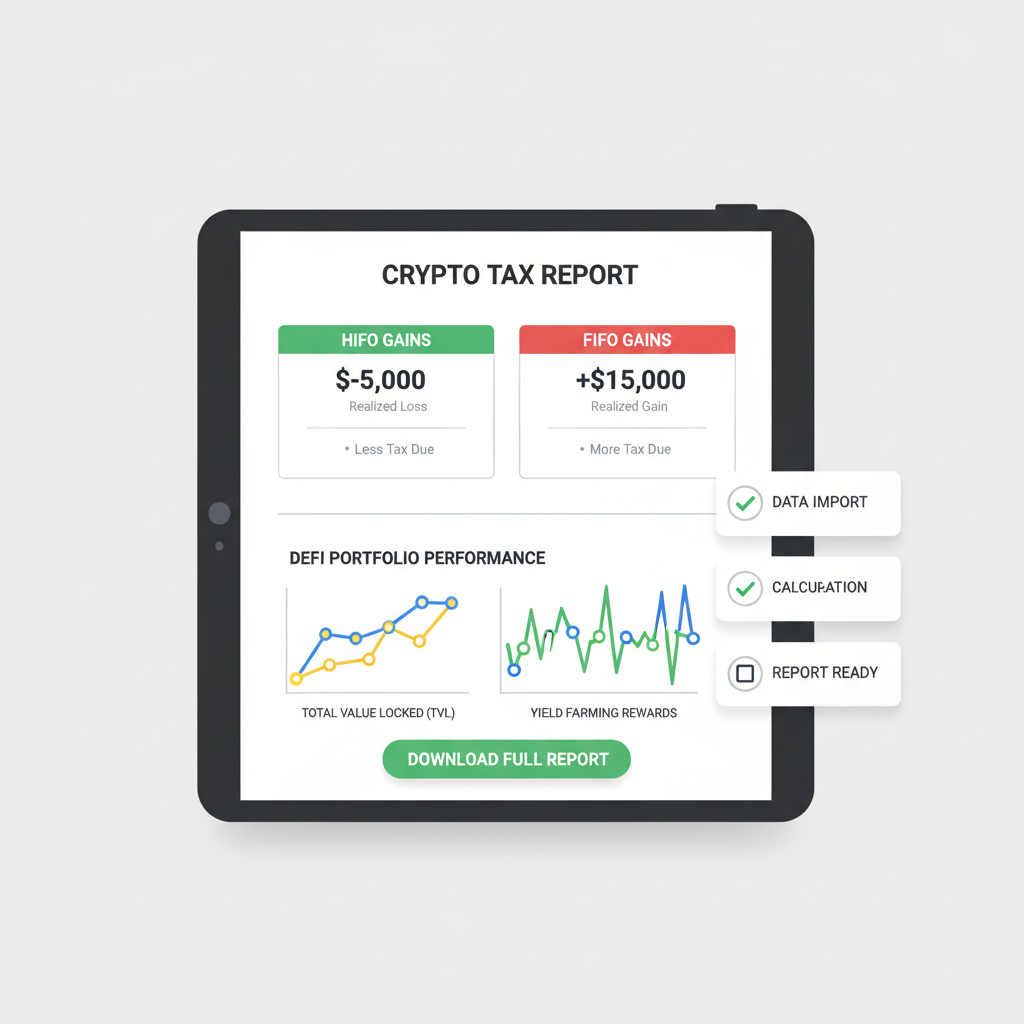

FIFO vs HIFO: Taxable Gains Comparison for DeFi Liquidity Provision Deposit (2 ETH @ $4,500 FMV)

| Metric | FIFO | HIFO |

|---|---|---|

| ETH Lots Available | Jan 1, 2025: 1 ETH @ $1,500 Apr 1, 2025: 1 ETH @ $2,800 Jul 1, 2025: 1 ETH @ $3,200 | Same lots available |

| Lots Disposed (LP Deposit) | Jan 1 (1 ETH @ $1,500) Apr 1 (1 ETH @ $2,800) | Jul 1 (1 ETH @ $3,200) Apr 1 (1 ETH @ $2,800) |

| Total Cost Basis | $4,300 | $6,000 |

| Fair Market Value (Proceeds) | $9,000 (2 ETH x $4,500) | $9,000 (2 ETH x $4,500) |

| Taxable Gain | $4,700 | $3,000 |

| HIFO Advantage vs FIFO | Baseline | ↓ $1,700 gain (36% reduction)* |

Why FIFO Bites Hardest in DeFi Liquidity Pools

FIFO's rigidity clashes with DeFi's churn. Yield farmers rotate positions rapidly; earliest lots often carry dirt-cheap bases from 2021 dips. Exiting a Uniswap pool? FIFO pairs that with peak withdrawal values, birthing outsized gains. Data from CoinTracker underscores this: in rising markets, FIFO yields 20-50% higher taxes versus optimized methods. For uniswap tax calculation, it's a drag on compounding.

Consider a stylized scenario: You deposit 1 ETH bought at $2,000 and another at $3,500 into a pool. Pool value doubles on withdrawal. FIFO sells the $2,000 lot first, taxing the full appreciation; HIFO flips it, minimizing the hit. Real DeFi traders I've advised slash liabilities 30% this way, redirecting savings to bolder positions.

HIFO Unleashed: Specific ID as Your DeFi Tax Weapon

Highest In, First Out via Specific Identification isn't a loophole; it's IRS-sanctioned precision. Highest-cost lots disposed first erode gains fastest, ideal for layered buys in volatile pools. BPM's accounting best practices spotlight HIFO's edge: it systematically curtails taxes, freeing capital for reinvestment.

Implementation demands discipline. Log each lot's acquisition details in tools supporting DeFi protocols. Platforms like those reviewed by InsideCryptoReview handle 500 and protocols, automating hifo liquidity pool taxes. For yield farming, tag LP tokens separately; their basis stems from underlying pair values at mint. Withdrawals dispose both LP and received tokens, so HIFO across wallets optimizes holistically.

Strategically, layer buys during dips to stock high-basis lots for future sales. This hybrid approach, blending FIFO compliance with HIFO opportunism, fortifies diversified DeFi portfolios against audits.

Layering isn't guesswork; it's a calculated strike against FIFO's drag. Pair it with real-time defi tax calculator tools that dissect liquidity events across 500 and protocols, and you're armored for 2026 filings. These platforms don't just compute; they simulate FIFO versus HIFO outcomes, spotlighting wallet-specific optimizations before you commit.

Wallet-by-Wallet Warfare: Tracking DeFi Positions in Silos

The IRS's wallet-by-wallet mandate fragments your empire into defensible forts. Each DeFi wallet or exchange account stands alone for cost basis, impervious to cross-pollination. A Uniswap V3 position in Wallet A can't offset losses from SushiSwap in Wallet B under FIFO. This silos strategy: dedicate high-volume yield farms to fresh wallets stocked with premium-basis tokens, reserving legacy low-basis holds for long-term HODL. I've seen clients halve effective rates by ring-fencing positions this way, turning compliance into competitive edge.

Impermanent loss harvesting fits here too. Crystallize losses strategically within HIFO frameworks, offsetting gains elsewhere. But precision rules: document pool compositions at deposit, track fee accruals separately, and value LP tokens at fair market upon burn. Messy chains like Arbitrum or Base demand chain-specific tools; generic spreadsheets crumble under DeFi's volume.

Master HIFO Specific ID: DeFi LP Tax Optimization Guide 2026

Mastery starts with selecting a calculator attuned to DeFi's chaos. Look for 250 and blockchain support, smart contract parsing for LP mints/burns, and HIFO simulations per wallet. These engines ingest CSV exports from Zapper or DeBank, outputting IRS-ready Form 8949 schedules. Run FIFO baselines first, then toggle to Specific ID; the delta often stuns, revealing untapped savings.

Real-World DeFi Scenarios: FIFO vs HIFO Payoff

Let's drill into Uniswap V2 ETH-USDC provision. You deposit 1 ETH at $3,000 (bought at $2,500 FIFO basis) and $3,000 USDC (basis $1 each). Pool appreciates 50% on withdrawal, but impermanent loss clips 10%. FIFO taxes the full ETH gain spread over oldest lots; HIFO pairs the highest ETH basis ($3,200 recent buy), trimming liability by 40%. Scale to $100K pools across five wallets, and you're shielding tens of thousands annually.

For yield farming marathons, compound effects amplify. Staking LP tokens in farms like Convex triggers nested dispositions; HIFO cascades downward, minimizing each layer. My hybrid portfolios blend 60% HIFO-optimized liquidity with 40% FIFO-stable HODLs, weathering audits while compounding yields. Data from Kryptos. io echoes this: disciplined Specific ID users report 25% average tax reductions versus FIFO defaults.

2026's Form 1099-DA influx from brokers underscores urgency. Centralized exchanges feed FIFO data directly to IRS; DeFi's decentralized nature falls on you. But that's opportunity: self-custody wallets under Specific ID evade broker presumptions, granting HIFO freedom. Pro tip: timestamp records on-chain via tools like Nansen for audit-proofing.

Empower your DeFi playbook with relentless tracking and method mastery. FIFO may dominate headlines, but HIFO-wielding liquidity providers dictate their tax destiny. Diversify positions, silo wallets, simulate relentlessly, and watch compliance fuel conquests in this relentless market.

No comments yet. Be the first to share your thoughts!