Understand the 2026 broker reporting rules

The 2026 tax season introduces a significant shift in how digital asset transactions are reported to the IRS. Brokers are now required to issue Form 1099-DA, creating a data trail that was previously fragmented. This change transforms crypto and NFT trading from a largely unreported activity into a highly visible one, increasing the stakes for accurate record-keeping.

The arrival of Form 1099-DA does not eliminate the need for manual tracking. While centralized exchanges will report your trades, many transactions—such as those on decentralized platforms, NFT swaps on non-custodial wallets, or airdrops received from unregulated sources—will not appear on any tax form. The IRS expects you to report all taxable events, regardless of whether a broker filed a form for them.

To stay compliant, you must reconcile the data you receive with your own transaction history. Start by gathering all 1099-DA forms from your brokers. Then, cross-reference these with your personal wallet records. Any transaction missing from the broker forms but present in your wallet is a taxable event you must still report. Failure to do so risks an audit, especially as the IRS continues to refine its data-matching capabilities for digital assets.

Calculate basis for staking rewards and airdrops

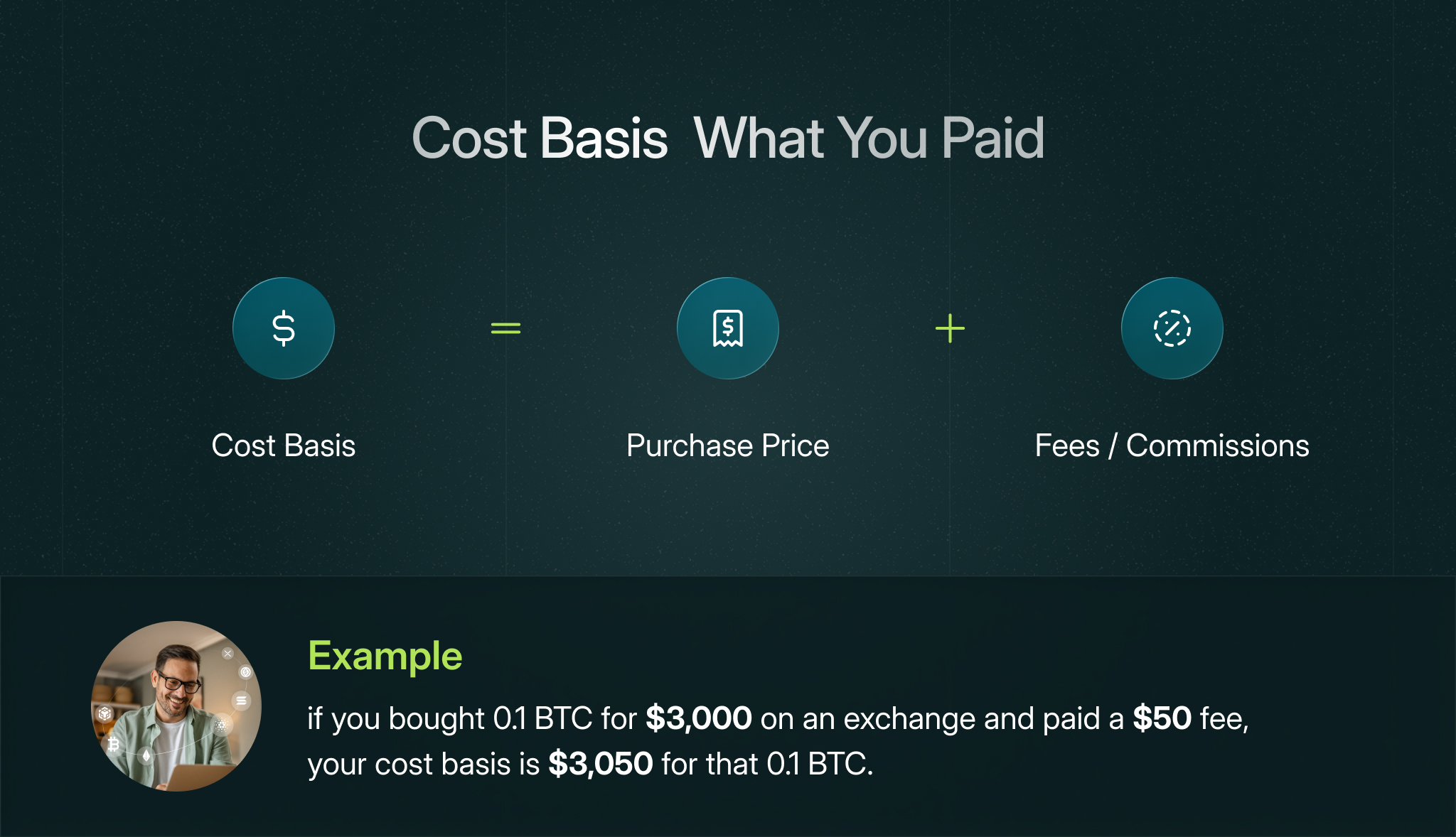

When you receive an NFT through staking or an airdrop, the IRS treats it as ordinary income. The value of that NFT on the day you receive it becomes your cost basis. This number is the foundation for every future tax calculation. If you get this wrong, your gains or losses will be incorrect, potentially triggering audits or penalties.

Treating these NFTs as property rather than currency simplifies the process. You are not taxed on the receipt itself as a capital event; you are taxed on the value as income. When you eventually sell or trade that NFT, you compare the sale price against the basis you recorded at receipt. The difference is your capital gain or loss.

Record the fair market value at receipt

Your first task is to determine the fair market value (FMV) of the NFT at the exact moment you gained control of it. Use a reliable, decentralized price oracle or a major exchange listing price from that specific date. Do not use the price from when you sold it.

If the NFT was not listed on any exchange, you may need to use a comparable sales data point from a marketplace like OpenSea or Blur. Document the source of this valuation. The IRS expects a reasonable good-faith estimate if an exact market price is unavailable, but you must be able to justify the number.

Store transaction hashes and timestamps

Proof is everything. You must store the transaction hash (txid) and the precise timestamp of the block where the NFT was transferred to your wallet. This data links your income event to the blockchain. Without these records, you cannot prove the date or value to the IRS if questioned.

Track basis in your tax software

Import this data into your crypto tax software or ledger. Most platforms allow you to manually add "income" events. Input the date, the FMV, and the transaction hash. This sets your cost basis for that specific NFT. When you later record a sale or swap, the software will automatically calculate the gain or loss based on this established basis.

Locate the block timestamp or transaction date when the NFT first appeared in your wallet. This is your income date.

Check a reputable exchange or marketplace for the NFT's price in USD at that exact date and time. Record this number.

Copy the transaction ID from a block explorer. This serves as your permanent proof of the event's existence and timing.

Add a new income event in your tax software. Input the FMV as your cost basis. This ensures accurate capital gains calculations later.

Track cross-chain swap basis adjustments

Bridging an NFT from Ethereum to another blockchain creates a distinct tax complication. When you move an asset across chains, the original transaction history does not automatically follow the token to the new ledger. This breaks the chain of custody required for accurate cost basis calculation, creating a high risk of reporting errors that can trigger IRS penalties.

The IRS treats the act of bridging as a potential disposal of the original asset. To maintain compliance, you must calculate the gain or loss on the source chain before the transfer completes. This requires precise tracking of the original purchase price, any transaction fees paid on the source network, and the fair market value at the moment of the bridge initiation.

Without this step, your cost basis on the destination chain is effectively reset to zero or an incorrect value. When you eventually sell the NFT on the new chain, you may face double taxation or an inflated capital gains liability because the original acquisition cost was lost in the transition.

Compare same-chain swaps vs. cross-chain bridges

The tax treatment differs significantly depending on whether you are swapping tokens on the same network or bridging across different ones. Understanding this distinction is critical for avoiding unexpected tax liabilities.

Proper documentation is your primary defense against IRS scrutiny. Keep detailed records of the bridge transaction hashes, the exact time of transfer, and the valuation data used for the basis calculation. If you are waiting for delayed broker reporting, such as the upcoming 1099-DA, ensure your internal records are complete to file an extension if necessary.

Failure to track these adjustments accurately can lead to significant financial consequences. The IRS has increased its focus on cryptocurrency and digital asset compliance, and errors in cross-chain transactions are a common audit trigger. Treat every bridge as a taxable event and maintain rigorous records to protect your assets.

File your return using tax software

Manual entry for NFT transactions is a recipe for errors and audits. The IRS treats digital assets as property, meaning every swap, airdrop, and staking reward is a taxable event. Tax software automates the aggregation of this data from multiple wallets and exchanges, ensuring you report accurately and avoid penalties for underreporting crypto income.

Start by connecting your wallets and exchange accounts. Most reputable platforms support direct API imports from major exchanges and blockchain explorers for NFT marketplaces. This step pulls transaction history directly, reducing the risk of omitting trades or misclassifying income. Be sure to reconcile imported data against any 1099-DA forms you receive from brokers to catch discrepancies early.

Once your data is imported, review the tax implications for each transaction. The software will calculate capital gains or losses based on your cost basis. For NFTs, this includes tracking the original purchase price and any associated gas fees. If you are waiting for delayed 1099-DA forms, file IRS Form 4868 for an automatic six-month extension to avoid late-filing penalties.

Connect your wallets and exchange accounts via API or CSV upload. Ensure all NFT marketplaces and DeFi protocols are included to capture every taxable event.

Cross-reference imported data with 1099-DA forms. Verify that cost basis calculations are correct and that no transactions were missed during the import process.

Select the appropriate tax forms (e.g., Schedule D, Form 8949) based on your transaction types. Export the final report and attach it to your tax return.

Common NFT tax questions for 2026

The tax implications of digital assets require precision. The IRS treats NFTs as property, meaning every swap, sale, or airdrop triggers a taxable event. Ignorance of these rules does not exempt you from penalties; the agency expects accurate reporting on your return.

Are NFTs still a thing in 2026?

NFTs have matured from speculative hype into long-term digital infrastructure. While the get-rich-quick era has passed, utility-driven projects continue to generate taxable income. If you hold or trade NFTs for utility or investment, they remain fully subject to current tax laws.

Do you have to pay taxes on NFTs?

Yes. The IRS classifies NFTs as property, similar to stocks or real estate. Buying, selling, or trading them can result in capital gains tax. In some cases, the IRS may treat an NFT as a collectible, which carries a maximum 28% tax rate on long-term gains, rather than the standard capital gains rates.

Is the IRS delay crypto tax until 2026?

No, the tax liability exists regardless of reporting delays. If you are waiting for a delayed 1099-DA from a broker, you must still report your transactions. File IRS Form 4868 to receive an automatic six-month extension until October 15, 2026, ensuring you have time to gather accurate records before finalizing your return.

How much will you be taxed in 2026?

Tax rates depend on your holding period and total income. Short-term gains (held less than 12 months) are taxed at your ordinary income tax rates, ranging from 10% to 37%. Long-term gains (held over 12 months) typically see lower rates of 0%, 15%, or 20%, though collectible NFTs may be taxed at up to 28%.

No comments yet. Be the first to share your thoughts!