Understand 2026 IRS reporting changes

The 2026 filing season introduces a structural shift in how the IRS tracks digital asset transactions. For the first time, mandatory broker reporting via Form 1099-DA requires exchanges to transmit cost-basis and gain/loss data directly to the federal government. This move ends the era of self-reporting for transactions occurring on or after January 1, 2026, fundamentally changing how NFT owners must track their holdings.

The transition creates a high-stakes environment for accuracy. As noted by digital asset tax experts, the 2026 filing season is likely to be "messy" and a "minefield" for investors who have not established rigorous tracking protocols [1]. The IRS will receive detailed data from brokers, meaning discrepancies between your reported figures and the data on file will trigger automated audits.

Manual calculation is no longer a viable safety net. The new rules require precise matching of acquisition dates and costs against sale proceeds. Failure to maintain accurate records before the 2026 deadline can result in significant penalties, as the IRS will assume the highest possible gain if basis cannot be substantiated [2].

Calculate your NFT capital gains

The IRS treats NFTs as property, not currency. This means every sale, trade, or exchange triggers a taxable event. To determine your exact liability, you must calculate the capital gain for each transaction individually.

The core formula is simple: Sale Price minus Cost Basis. The cost basis includes the original purchase price plus any transaction fees paid to mint or acquire the asset. The sale price is what you received, minus any fees paid during the disposal.

Step 1: Determine your cost basis

Your cost basis is the total amount you invested to acquire the NFT. This includes:

- The price paid in crypto or fiat currency.

- Gas fees or network transaction fees paid at the time of purchase.

- Marketplace fees if they were part of the acquisition cost.

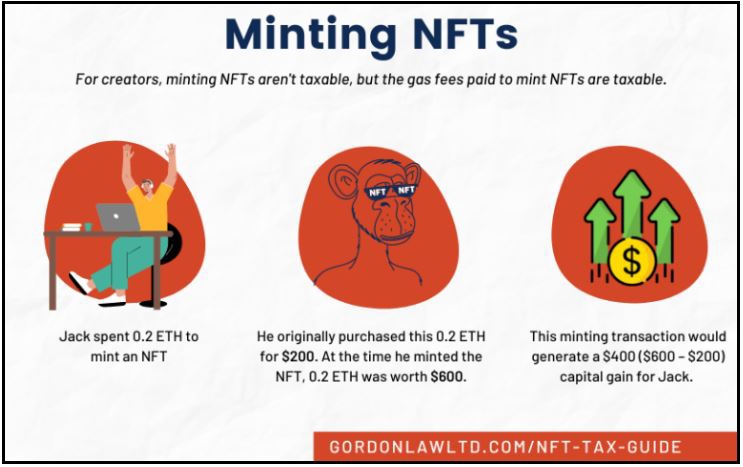

If you minted the NFT yourself, your basis is typically the gas fees paid to the blockchain, assuming the mint price was zero. If you bought it on a marketplace like OpenSea, add the purchase price and the gas fees to your basis.

Step 2: Calculate the gain or loss

Subtract your cost basis from your sale price.

- Gain: If the sale price is higher than your basis, you have a capital gain.

- Loss: If the sale price is lower, you have a capital loss, which can offset other gains.

For example, if you bought an NFT for 0.5 ETH ($1,000) plus $20 in gas, your basis is $1,020. If you sell it for 0.6 ETH ($1,200) minus $10 in gas, your net sale price is $1,190. Your gain is $1,190 - $1,020 = $170.

Step 3: Classify as short-term or long-term

The holding period determines your tax rate. The IRS distinguishes between short-term and long-term capital gains based on how long you held the asset.

- Short-term: Held for one year or less. These gains are taxed at your ordinary income tax rates, which range from 10% to 37% for 2026.

- Long-term: Held for more than one year. These qualify for reduced capital gains rates of 0%, 15%, or 20%, depending on your total taxable income.

Track your acquisition and disposal dates carefully. If you trade an NFT for another NFT, the holding period for the new asset begins on the day of the trade. For detailed guidance, refer to IRS Notice 2014-21, which confirms virtual currency is treated as property.

Track transactions across multiple wallets

If you trade NFTs across Ethereum, Solana, or Polygon using different browser wallets, your tax liability is hidden in plain sight. The IRS does not see your wallets as a single entity; they see disconnected ledgers. Without aggregation, you will likely miss cost basis data or misreport gains, turning a manageable filing into a "minefield" for 2026, as noted by digital asset tax experts in Forbes.

To track transactions across multiple wallets accurately, you must move beyond manual spreadsheets. Use dedicated NFT tax software that connects to all your wallet addresses via read-only API keys or public address imports. These tools pull on-chain data from every chain you use, merging the fragmented history into one unified ledger. This aggregation is the only way to catch cross-chain swaps or bridging events that often trigger taxable events.

Once your data is aggregated, verify the completeness of your records before filing. Ensure every buy, sell, and swap is accounted for. Use this checklist to verify your data integrity:

-

All active wallet addresses are imported into the tax software.

-

Transaction history covers the full tax year (January 1 to December 31).

-

Cross-chain bridge transactions are identified and classified correctly.

-

Cost basis for each NFT is calculated using a consistent method (e.g., FIFO).

-

Internal transfers (wallet-to-wallet) are marked as non-taxable.

Proper tracking ensures your NFT tax reporting aligns with IRS requirements for cost basis and gain/loss data, which begin in earnest for 2026 filings. Skipping this step leaves you vulnerable to audits and incorrect tax bills.

Avoid common NFT tax mistakes

Tracking NFT transactions requires precision. A single overlooked detail can trigger an audit or result in overpaying. The following pitfalls are the most frequent errors creators and collectors make when filing returns.

Ignoring gas fees in your cost basis

Many traders calculate profit simply by subtracting the purchase price from the sale price. This ignores transaction costs. Gas fees paid to mint, buy, or sell an NFT are part of your cost basis. They reduce your taxable gain. If you fail to include these fees, you report higher income than you actually earned.

Keep a ledger of every transaction fee. When you sell, subtract the original mint price, the purchase gas fee, and the sale gas fee from your proceeds. This ensures your reported gain reflects the true net profit.

Misclassifying creator royalties

Royalties are not capital gains; they are ordinary income. If you mint and sell an NFT, the royalty fee is compensation for your work. It is taxed at your marginal income tax rate, which can be significantly higher than the capital gains rate. Treating royalties as long-term capital gains is a common error that can lead to underpayment penalties.

Report royalty income as self-employment income or ordinary income in the year you receive it. Do not wait until you sell the NFT to report it. This distinction is critical for accurate tax liability.

Missing the wash-sale gap

The IRS does not currently apply wash-sale rules to cryptocurrencies or NFTs. This means you can sell an asset at a loss and immediately repurchase it to claim that loss on your taxes. While this is a legal strategy, it is a frequent source of confusion. Many investors assume the rule applies because it does for stocks, leading them to miss out on valid tax-loss harvesting opportunities.

Document your sales and repurchases carefully. If you sell an NFT at a loss and buy it back within 30 days, you can still deduct the loss. However, keep clear records to prove the transaction sequence in case of an audit.

Prepare your NFT tax return for 2026

Start by gathering every record of your NFT transactions. You need the date acquired, date sold, proceeds from the sale, and your cost basis for each item. The IRS treats NFTs as property, so you must report every sale, trade, or exchange, even if the platform didn’t issue a tax form. If you traded NFTs across different wallets or marketplaces, consolidate those records into one master spreadsheet before you begin.

Next, fill out Form 8949 to list each individual transaction. This form captures the details of your sales and trades. If you have more than a handful of transactions, consider using tax software that imports directly from your wallet or exchange data. This reduces the risk of manual entry errors, which are common when dealing with high-volume trading.

Once Form 8949 is complete, transfer the totals to Schedule D. This section summarizes your capital gains and losses for the year. If your total gains exceed $3,000, they will offset your ordinary income up to that limit, with any remaining loss carried forward to future years. Double-check that your cost basis calculations align with the IRS guidance on digital assets.

Finally, review your return for common pitfalls. Did you forget to report NFTs received as mining rewards or staking income? These are taxable as ordinary income at their fair market value when received. If your situation involves complex trades, foreign exchanges, or significant gains, consult a CPA or tax professional specializing in digital assets to ensure compliance.

Nft tax 2026: frequently asked: what to check next

Are NFTs still worth anything in 2026?

NFTs have evolved beyond the 2021 hype into practical applications and niche markets. As of 2026, the space rewards knowledge over speculation. Whether NFTs fit your strategy depends on your goals and risk tolerance. Source

How are NFT sales taxed?

The IRS generally taxes NFTs as property, similar to cryptocurrencies like Bitcoin or Ethereum. Gains from the sale of NFTs are typically taxable. If you dispose of NFTs after less than 12 months of holding, they are taxed at short-term capital gains rates, which range from 10% to 37% depending on your income bracket.

Do NFT creators pay different taxes?

Yes. While collectors pay capital gains tax on sales, NFT creators often face ordinary income tax rates on their earnings, which can reach up to 37%. Royalties and initial sales are treated as self-employment income, potentially leading to a higher effective tax rate compared to simple trading gains.

What happens if I lose my NFT keys?

Losing access to your NFT wallet means you cannot prove ownership or cost basis to the IRS. Without transaction records or wallet history, you cannot claim losses or calculate gains. Always back up your seed phrases and maintain detailed transaction logs to ensure compliance.

Work through NFT Tax Rules

No comments yet. Be the first to share your thoughts!