Understand the 2026 reporting shift

The 2026 filing season marks a structural change in how the IRS tracks digital collectibles. For years, NFT traders operated in a reporting gap, relying on personal records to calculate gains and losses. That era ends with the introduction of Form 1099-DA.

Form 1099-DA standardizes digital asset reporting across exchanges and marketplaces. By mid-February 2026, you should receive this form from any broker that facilitated your NFT transactions MetaMask, 2026. The form details your cost basis, proceeds, and resulting gain or loss for the tax year.

This shift eliminates the "wash sale" ambiguity that previously plagued many collectors. You no longer need to reconstruct transaction histories from scattered wallet logs if your trades occurred on reporting-compliant platforms. The data is now pushed to the IRS, meaning discrepancies between your return and their records are flagged faster.

If you traded on non-custodial wallets or decentralized exchanges that do not issue Form 1099-DA, you remain responsible for accurate self-reporting. However, for the majority of traders using major marketplaces, the new form provides a clear starting point for your NFT tax 2026 calculations. Always compare the 1099-DA against your own records to catch errors before filing.

Gather your transaction records

Before you can calculate your NFT tax 2026 liability, you need a complete ledger of every digital collectible event. The IRS treats NFTs as property, meaning every swap, sale, and trade triggers a taxable event. If your records are fragmented across multiple platforms, you will likely underestimate your gains or overpay due to missing loss deductions.

Start by exporting data from every exchange, wallet, and marketplace you used. Most major platforms allow you to download CSV transaction histories. Look for fields like date, asset type, transaction type (buy, sell, trade, mint), and USD value at the time of the event.

Log into exchanges like OpenSea, Rarible, or crypto exchanges that support NFT trading. Go to the transaction history or tax report section. Filter for the current tax year and download the CSV file. Ensure you capture all "sell" and "trade" events, as these determine your capital gains or losses.

For non-custodial wallets like MetaMask or Phantom, use blockchain explorers or portfolio trackers to generate transaction lists. Since these platforms don’t issue consolidated tax forms, you must manually reconcile on-chain data. Look for incoming transfers that might constitute income (like airdrops or rewards) and outgoing transfers that represent sales.

Once you have your private records, compare them against any IRS Form 1099-DA or similar broker statements you receive. Starting in 2026, cost basis and gain/loss data reporting for digital assets becomes more standardized. Any discrepancy between your records and the IRS forms must be resolved before filing to avoid audits.

Keep these exports organized in a single folder. You will need them to fill out Schedule D and Form 8949 of your tax return. Missing even a single trade can lead to inaccurate reporting, so thoroughness here is your best defense against future compliance issues.

Calculate gains and losses per asset

To file your NFT tax 2026 return accurately, you must separate your activity into two distinct buckets: capital gains for collectors and ordinary income for creators. The IRS treats these transactions differently, and mixing them up is a common audit trigger. You need to calculate the profit or loss for every single NFT transaction based on its specific holding period.

Collector gains: short-term vs. long-term

When you sell an NFT for more than you paid, the difference is a capital gain. The tax rate depends on how long you held the asset before selling it.

| Holding Period | Tax Rate | Description |

|---|---|---|

| One year or less | Ordinary income rates (10%-37%) | Short-term capital gains. Taxed at your standard marginal rate. |

| More than one year | 0%, 15%, or 20% | Long-term capital gains. Rates depend on your total taxable income. |

For example, if you bought an NFT in January 2025 and sold it in March 2026, the profit is taxed as a short-term gain. If you held it until April 2026, it qualifies for the lower long-term rates. You must track the exact acquisition and disposal dates for each token to apply the correct rate.

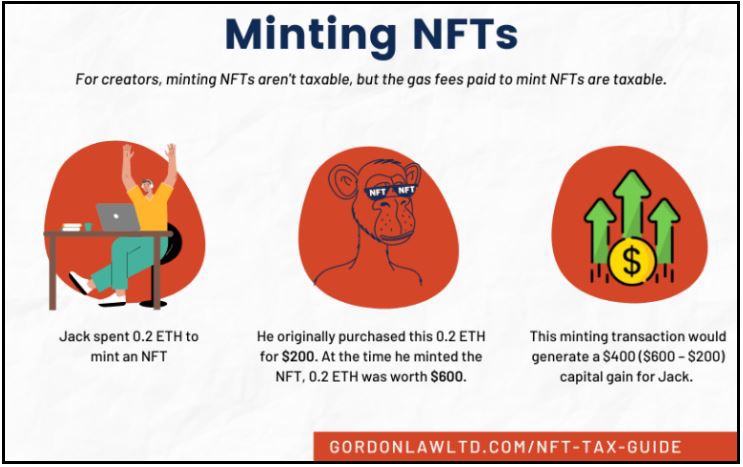

Creator royalties: ordinary income

If you mint and sell your own NFTs, the rules change. Royalties and primary sales are treated as self-employment income, not capital gains. This means they are subject to ordinary income tax rates, which can reach 37%, plus the 15.3% self-employment tax.

Note: While collectors pay up to 28% on capital gains, creators face a brutal tax reality with rates up to 50% when combining income and self-employment taxes. This is a critical distinction for artists entering the 2026 filing season. LinkedIn

Do not try to offset creator income with collector losses unless they are part of the same trade or business. The IRS generally views these as separate activities. Keep your creator income separate in your accounting software to avoid confusion during an audit.

Handling cost basis

Your cost basis is what you paid for the NFT, including transaction fees. If you received an NFT as a gift, your basis is usually the donor’s original cost. If you mined or earned it through staking, your basis is the fair market value at the time of receipt.

When calculating your gain, subtract your cost basis from the sale price. If you sold the NFT for less than you paid, you have a capital loss. You can use these losses to offset your capital gains. If your losses exceed your gains, you can deduct up to $3,000 against your ordinary income each year.

- Verify holding periods: Check the blockchain transaction dates to confirm if each NFT qualifies for long-term rates.

- Categorize income types: Separate collector sales (capital gains) from creator royalties (ordinary income).

- Reconcile records: Match your personal logs with any 1099-DA forms received from exchanges to ensure no transactions are missed.

Use a checklist to verify these details before filing. The 2026 filing season is expected to be complex, with stricter reporting requirements from digital asset platforms. Being organized now prevents costly errors later. Forbes

File Form 8949 and Schedule D

Reporting your NFT tax 2026 liabilities requires mapping your digital collectible transactions to IRS Form 8949 and Schedule D. This process translates blockchain activity into the standardized format the IRS uses to track capital gains and losses.

The 2026 filing landscape introduces a significant change: the arrival of Form 1099-DA for digital asset broker transactions. Brokers will now issue this form to report sales, exchanges, and transfers, providing a direct link between your on-chain activity and your federal return. You must reconcile the data on this form with your personal records to ensure accuracy.

Collect all records of your NFT sales, trades, and transfers. If you used a marketplace that acts as a broker, locate the Form 1099-DA or equivalent tax document they provided. For peer-to-peer transactions, export your transaction history from your wallet or aggregator tools.

List each disposition of digital collectibles on Form 8949. Enter the date acquired, date sold or disposed of, proceeds (sale price), and cost basis. If you received a 1099-DA, check the box to indicate the transaction was reported to the IRS to avoid double-counting errors.

Move the totals from Form 8949 to Schedule D (Form 1040). This form calculates your overall net capital gain or loss from all investments, including your NFT activities. Ensure short-term and long-term holdings are categorized correctly based on how long you held each collectible.

The deadline for American taxpayers to file these forms for the 2025 tax year is April 15, 2026. Expatriates have an extended deadline of June 15, 2026. Missing these dates can result in penalties that outweigh the tax liability itself.

Common NFT tax mistakes to avoid

Filing your NFT tax 2026 returns requires precision. Digital asset experts warn that the 2026 filing season is a "minefield" for investors who treat crypto reporting casually [1]. Small oversights can trigger audits or unexpected liabilities.

Ignoring airdrops and free mints

Many collectors assume that NFTs received for free have no tax basis. The IRS treats airdrops and free mints as taxable income at their fair market value when received. If you received an airdrop worth $500, that amount is added to your gross income. Failing to report these events is a common error that leaves a gap in your tax record.

Misclassifying creator royalties

Creators face a different tax reality than collectors. While collectors pay capital gains tax on sales, creators often pay ordinary income tax on royalties [2]. In 2026, these royalties may be classified as self-employment income, pushing tax rates up to 37% plus self-employment tax. Misclassifying this income as capital gains can result in significant penalties during an audit.

Overlooking DeFi interactions

Interacting with decentralized finance protocols involving NFTs can create taxable events. Staking an NFT in a liquidity pool, lending it, or using it as collateral may trigger income recognition or capital gains calculations. These interactions are often invisible to standard exchange reports, so you must track them manually to ensure your NFT tax 2026 filing is accurate.

No comments yet. Be the first to share your thoughts!