What changed for NFT taxes in 2026

The 2026 filing season introduces mandatory broker reporting for digital assets, requiring centralized exchanges to submit cost basis and gain/loss data directly to the IRS. This shift eliminates the previous advantage of unreported on-chain transactions, making accurate compliance essential for anyone trading NFTs through regulated platforms.

Step 1: Gather your transaction history

Before calculating liability, compile a complete ledger of all NFT activity. The IRS treats NFTs as property, meaning every swap, sale, or purchase is a taxable event. Relying on incomplete records risks underreporting income or missing cost basis data, which can trigger audits.

Export from centralized exchanges

Centralized exchanges like Coinbase, Kraken, or Binance provide the most straightforward data. Log in to your account and go to the tax or transaction history section. Download the full CSV report for the relevant tax year, ensuring you capture all trading pairs, including swaps where you exchanged Ethereum or Solana for an NFT.

Export from decentralized marketplaces

Marketplaces like OpenSea, Blur, and Magic Eden often lack consolidated tax reports. You may need to export transaction logs directly from your wallet or use a portfolio tracker. For OpenSea, check account settings for a "Transaction History" export. If these options are unavailable, aggregate wallet data manually or use crypto tax software that syncs with your wallet address.

Consolidate wallet transactions

Personal wallets (MetaMask, Phantom, Ledger) hold raw on-chain data. While block explorers like Etherscan or Solscan show history, their exports are difficult to read for tax purposes. Import your wallet address into a tax calculation tool to automatically categorize transactions as sales, swaps, or transfers, saving you from manually parsing blockchain entries.

Verify NFT purchases

Buying an NFT is a taxable event because you are exchanging cryptocurrency for property. Many users overlook this, assuming only sales are reportable. Check your history for NFT purchases made with crypto and record the value of the cryptocurrency at the time of purchase to establish your cost basis. For example, if you bought an NFT for 1 ETH when ETH was worth $2,000, your cost basis is $2,000.

Organize your data

Once exported, organize data into a single spreadsheet or import it into tax software. Group transactions by type: sales, purchases, swaps, and transfers. Flag unclear transactions, such as airdrops or staking rewards, for later review. A clean dataset makes the calculation phase faster and more accurate.

Step 2: Calculate cost basis and gains

Determining tax liability starts with establishing the original cost basis for each NFT. The IRS treats cryptocurrency as property, so every transaction involving crypto triggers a taxable event. When you buy an NFT using Ethereum, you are disposing of that cryptocurrency, requiring you to calculate the gain or loss on the crypto itself based on its value at the moment of purchase.

If you purchased an NFT with fiat currency, your cost basis is the amount paid plus transaction fees. Most NFT transactions involve crypto, which complicates the calculation. You must determine the value of the cryptocurrency at the exact time of the swap. For example, if you bought an NFT for 0.5 ETH and the value of 0.5 ETH was $1,500 at that time, your NFT’s cost basis is $1,500. If the ETH you spent had appreciated since you acquired it, you also owe capital gains tax on the ETH transaction itself.

Once you have the cost basis, compare it to the proceeds from any future sale or trade. Proceeds include the value of any cryptocurrency or fiat received upon disposal. If you traded the NFT for another digital asset, use the value of the received asset at the time of the trade. The difference between the proceeds and the cost basis is your capital gain or loss.

Holding period matters for tax rates. Gains from assets held for one year or less are taxed as short-term capital gains, aligned with your ordinary income tax bracket. Assets held longer than one year qualify for long-term capital gains rates, which are typically lower. Accurate record-keeping of dates and values is essential to apply the correct rate.

Distinguish creator income from sales

Not all NFT activity is taxed the same way. The IRS treats collectors and creators differently, meaning your tax bill depends entirely on your role in the transaction. Confusing these two categories can lead to underreporting income or overpaying taxes on capital gains.

Collectors: Capital Gains

When you buy an NFT to hold and later sell it for a profit, you are engaging in a capital asset transaction. This is treated like selling stocks or real estate. You pay capital gains tax on the difference between your sale price and your cost basis.

- Short-term gains: If you held the NFT for one year or less, profits are taxed as ordinary income, matching your highest marginal tax bracket.

- Long-term gains: If you held the NFT for more than a year, profits are taxed at lower long-term capital gains rates (0%, 15%, or 20%, depending on your income).

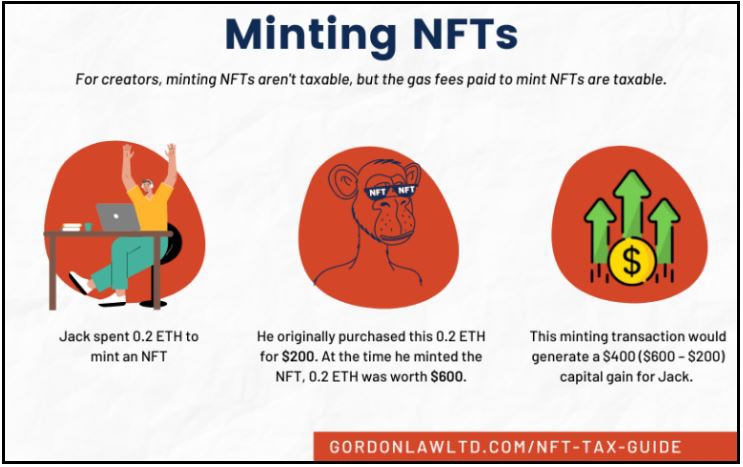

Creators: Ordinary Income

Creators face a different tax reality. When you mint an NFT or earn royalties from secondary sales, the IRS views this as self-employment income. This is ordinary income, not capital gains.

- Minting sales: The full sale price of your primary mint is taxable as self-employment income.

- Royalties: Every time your NFT resells, the royalty you receive is additional ordinary income.

- Tax rates: This income is subject to self-employment tax (Social Security and Medicare) plus ordinary income tax, which can reach up to 37% for high earners.

Side-by-Side Comparison

Use this table to quickly identify which tax rules apply to your specific NFT activity.

| Role | Transaction Type | Tax Type | Tax Rate |

|---|---|---|---|

| Collector | Selling held NFT | Capital Gains | 0-20% (long-term) or ordinary (short-term) |

| Creator | Minting primary sale | Self-Employment Income | Up to 37% + 15.3% SE tax |

| Creator | Earning royalties | Self-Employment Income | Up to 37% + 15.3% SE tax |

| Collector | Buying NFT | Cost Basis | N/A (no tax due at purchase) |

Common mistakes that trigger IRS audits

The 2026 filing season introduces new broker reporting rules that add layers of complexity to NFT tax compliance. The IRS is cross-referencing Form 1099-DA data against your returns, meaning discrepancies are no longer just errors—they are red flags. Ignoring the fine print on digital asset reporting can lead to audits that are costly and time-consuming to resolve.

One of the most frequent triggers is failing to report NFT transfers between your own wallets. While moving assets from one self-custody wallet to another is not a taxable event, the transaction still appears on the blockchain. If you do not properly label these transfers in your tax software, the system may flag them as sales, creating phantom income that requires manual correction during an audit.

Another critical pitfall is overlooking the new cost basis and gain/loss reporting requirements. Starting in 2026, brokers must report detailed transaction data to the IRS. If your NFT sales are processed through a centralized exchange, the data will match their records. However, if you traded on decentralized platforms or peer-to-peer, you must manually calculate and report your gains. Missing this data creates a mismatch that the IRS’s automated systems are designed to catch.

To avoid these pitfalls, treat your NFT tax preparation as a forensic audit of your own activity. Every transaction, whether taxable or not, needs a clear paper trail. Using specialized tax software that integrates with major exchanges and supports manual entry for DeFi interactions is essential for accuracy.

Frequently asked questions about NFT taxes

For official guidance, refer to the IRS Notice 2014-21 which establishes the foundational treatment of virtual currencies.

No comments yet. Be the first to share your thoughts!