Understand the 2026 reporting changes

The 2026 tax season marks a structural shift in how digital assets are reported. For the first time, the IRS is receiving standardized transaction data directly from digital asset brokers. This transition from informal self-reporting to formal broker reporting creates a "minefield" for most crypto and NFT investors, as noted by digital asset tax experts in recent industry analyses [src-serp-2].

The primary driver of this complexity is the new Form 1099-DA. This form requires digital asset brokers to report certain digital asset proceeds to both the IRS and the taxpayer. If you sold AI-generated art, traded metaverse land, or moved NFTs between wallets via a compliant exchange, your broker is now filing this form on your behalf. The IRS will have a record of your sales that you must reconcile with your own tax return.

This change impacts how you track your NFT tax liability. Previously, many traders relied on the "wash sale" loophole or failed to report small transactions. Now, the data trail is public to the IRS. You must ensure your internal records match the 1099-DA forms you receive from your exchanges. If you traded on decentralized platforms that do not report, you still bear the full burden of accurate self-reporting, but the gap between your records and the IRS's data is shrinking rapidly.

Classify your NFT transactions

To determine your correct tax rate, you must first identify whether the transaction counts as a capital gain or ordinary income. This distinction separates passive investors from active creators or traders.

For collectors, NFTs are generally treated as property. When you sell an NFT for more than you paid, you owe capital gains tax. If the asset was held for one year or less, it is short-term and taxed at your standard income rate. Holding it longer qualifies for long-term rates, which are typically lower. The IRS may classify high-value digital art as a "collectible," potentially applying a higher maximum rate of 28%.

Creators face a different reality. Revenue from minting and secondary sale royalties is considered self-employment income. This amount is subject to ordinary income tax, which can reach up to 37%, plus self-employment taxes. Unlike capital gains, there is no long-term holding period benefit for creator royalties. You must report this income on Schedule C.

| Transaction Type | Tax Classification | Typical Rate | Reporting Form |

|---|---|---|---|

| Collector Sale (Short-term) | Capital Gain | Ordinary Income Tax | Schedule D |

| Collector Sale (Long-term) | Capital Gain | 0%, 15%, or 20% | Schedule D |

| Creator Minting Revenue | Ordinary Income | Up to 37% + SE Tax | Schedule C |

| Creator Royalties | Ordinary Income | Up to 37% + SE Tax | Schedule C |

See IRS Notice 2014-21 for the foundational guidance on virtual currency as property.

Track your cost basis and sales

The 2026 tax season introduces Form 1099-DA, requiring brokers to report digital asset proceeds directly to the IRS. This shift changes how you track NFT taxes, but it does not eliminate the need for accurate cost basis reporting. Because liquidity is fragmented across decentralized exchanges, private wallets, and marketplaces, relying solely on broker statements will leave gaps in your filings.

You must aggregate transaction history wallet-by-wallet to ensure every sale, trade, and airdrop is accounted for. Think of your digital assets like a portfolio of physical assets in different safety deposit boxes; you cannot file a single inventory list unless you visit every box individually.

Follow this workflow to compile your data before preparing your tax return.

Log into each centralized exchange where you traded NFTs, such as OpenSea’s integrated fiat on-ramps or major crypto exchanges. Navigate to the transaction history or exports section and download the CSV or PDF records for the entire tax year. Ensure you capture all buy, sell, and trade events, as these records will form the baseline for your cost basis calculations.

For assets held in non-custodial wallets like MetaMask or Ledger, exchange exports will not exist. Use blockchain explorers like Etherscan or Solscan to review your wallet address history. Alternatively, use reputable portfolio trackers that can sync with your wallet address to generate a comprehensive transaction log. This step is critical for capturing decentralized exchange (DEX) swaps and direct peer-to-peer NFT transfers that bypass centralized brokers.

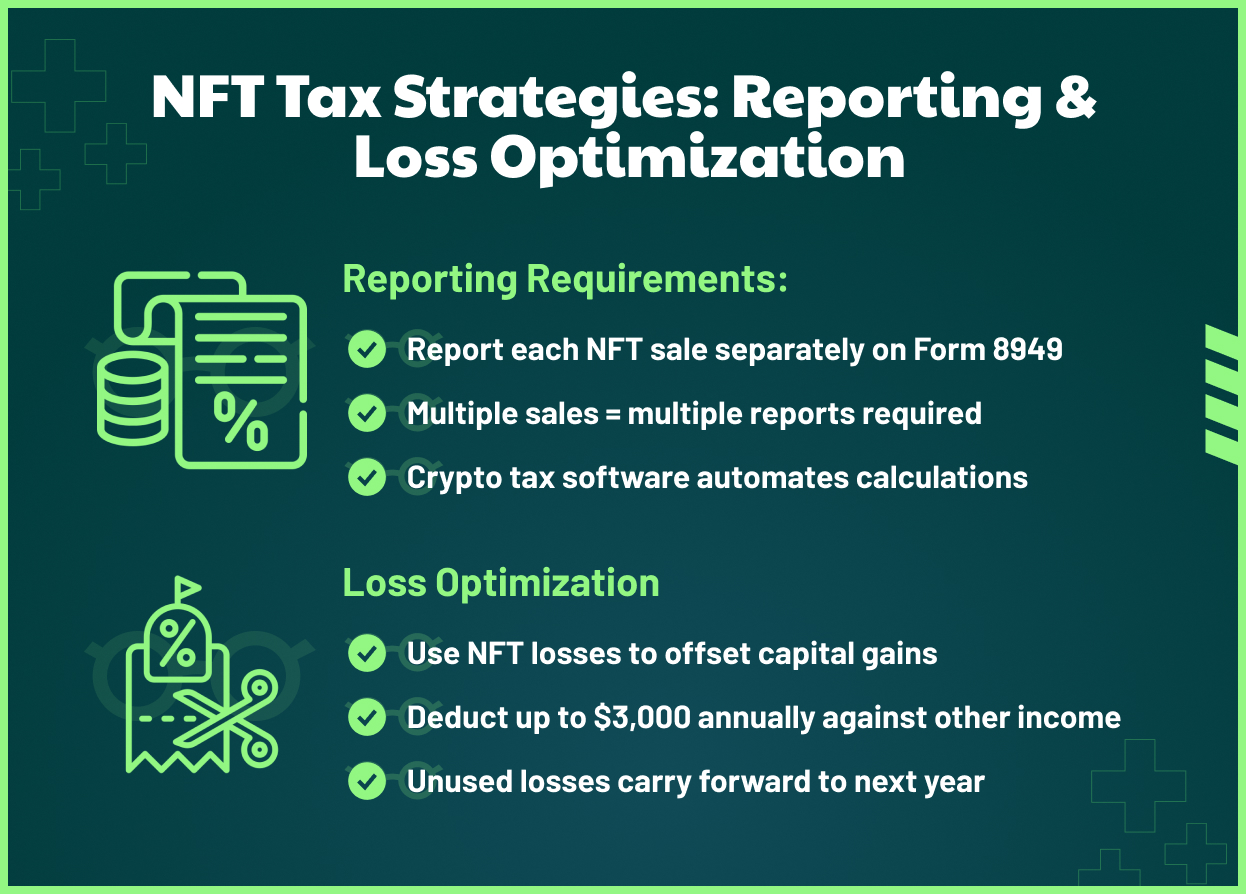

Match every sale event with its corresponding purchase event to determine your gain or loss. The IRS treats NFTs as property, so you must identify which specific NFT was sold if you hold multiple copies of the same collection. Use the FIFO (First-In, First-Out) method or specific identification method consistently. Record the fair market value in USD at the time of the sale and subtract your original cost basis to find the taxable amount.

Once you have your private records, compare them against the Form 1099-DA statements provided by your brokers. Look for discrepancies in reported proceeds or missing transactions. If your calculated gains differ from the broker’s report, you must be prepared to explain the difference to the IRS, typically by attaching Form 8949 with detailed explanations for any adjustments or exclusions.

Keeping a disciplined, wallet-by-wallet ledger is the only way to survive the increased scrutiny of 2026 tax reporting. Start gathering these exports now, before the filing deadline approaches.

Handle AI Art and Metaverse Specifics

Reporting NFTs requires distinguishing between traditional digital collectibles and two complex categories: AI-generated art and metaverse real estate. Both involve unique valuation and ownership questions that standard crypto reporting often misses.

AI Art: Proving Human Authorship

The IRS treats NFTs as property, but AI-generated works complicate this classification. If an algorithm creates the image with minimal human input, the work may not qualify for copyright protection, affecting its valuation as a capital asset.

- Document the Prompt and Process: Keep records of your prompts, iterations, and any manual editing. This proves your creative contribution, distinguishing your work from pure machine output.

- Establish Fair Market Value: Value the NFT at the time of creation or first sale. If you minted it yourself, the cost basis is often zero unless you paid for gas or platform fees.

- Report the Disposal: When you sell, report the gain or loss. Short-term gains (held under a year) are taxed as ordinary income, while long-term gains (over a year) receive preferential rates.

Metaverse Land: Real Estate or Digital Asset?

Metaverse land transactions often resemble real estate deals more than simple token swaps. Platforms like Decentraland or The Sandbox allow you to buy, sell, and lease parcels.

- Valuation Method: Treat land as a capital asset. Your cost basis includes the purchase price plus transaction fees. When you sell, subtract this basis from the sale proceeds to determine your gain.

- Leasing Income: If you lease land to another user, the rental income is taxable. Report this as ordinary income on your tax return, similar to physical real estate rentals.

- Improvements: Costs for building structures or adding features to your land may be capitalized, increasing your cost basis and reducing your taxable gain upon sale.

Practical Steps for Compliance

To ensure accurate reporting, follow this sequence for both AI art and metaverse transactions:

- Track Every Transaction: Use a crypto tax software that supports NFTs and metaverse platforms. Manual tracking is error-prone due to the volume of small transactions.

- Separate AI and Metaverse Data: Create distinct categories for AI art sales and metaverse land transactions. This helps auditors understand the nature of your income.

- Consult a Tax Professional: Given the evolving nature of AI and metaverse regulations, a professional can help you navigate specific IRS guidance and avoid penalties.

Note: The IRS has not issued specific guidance on AI-generated NFTs. Treat these assets with caution and document your process thoroughly to support your tax position.

Avoid common filing mistakes

The 2026 filing season is shaping up to be a minefield for NFT and digital asset holders. New reporting requirements and shifting interpretations of existing rules mean that small oversights can trigger audits or unexpected liabilities. Focus on these three specific pitfalls to keep your return accurate.

Ignore the 1099-DA reporting mandate

The most significant change for 2026 is the introduction of Form 1099-DA. Digital asset brokers will now report proceeds from sales directly to the IRS. If you trade on a major exchange, you will receive this form regardless of whether you made a profit or a loss. Do not assume that because you did not file a 1040-Schedule D previously, you are exempt now. The IRS will have the data; your job is to match your records to their numbers. Failure to report these transactions can result in penalties that far exceed the tax due.

Underreporting gas fees and transaction costs

Many creators and collectors forget that transaction fees (gas) are deductible or can reduce your cost basis. When you mint an AI-generated NFT or sell a piece in the metaverse, the gas fees paid to the network are part of the transaction cost. If you are selling, these fees reduce your gross proceeds. If you are minting, they add to your cost basis. Ignoring these small costs leads to an inflated profit figure and higher taxes. Keep a running log of all wallet interactions to capture these expenses accurately.

Misapplying wash-sale rules

Currently, the wash-sale rule—which prevents investors from claiming a loss on a security sold at a loss if you buy a "substantially identical" security within 30 days—does not apply to cryptocurrency or NFTs under federal tax law. However, this is a moving target. Legislative proposals and regulatory guidance are actively debating whether to extend these rules to digital assets. While you may currently claim a loss on a NFT that you repurchase within a month, relying on this loophole is risky. Treat every sale as a final event and consult a tax professional to understand how new proposals might impact your specific holdings in 2026.

Pre-filing checklist

Before you submit your return, verify these items to ensure compliance:

-

Reconcile all 1099-DA forms with your personal transaction logs.

-

Calculate cost basis including all gas fees for minting and selling.

-

Review recent legislative updates on wash-sale rule extensions.

-

Separate personal use NFTs (exempt) from investment NFTs (taxable).

Frequently asked questions about NFT taxes

[1] https://www.binance.com/en/square/post/35955840558193 [2] https://www.experian.com/blogs/ask-experian/how-are-nft-taxed/ [3] https://www.thebulldog.law/crypto-taxes-in-2026-what-investors-need-to-know

No comments yet. Be the first to share your thoughts!