Get nft tax 2026 right

Before you start calculating capital gains or losses, you need to sort your records. The 2026 filing season is shaping up to be messy, with experts calling it a "minefield" for crypto investors due to new DeFi reporting rules and stricter IRS scrutiny. If you skip the setup, you will spend weeks untangling errors later.

Start by gathering every transaction record. This includes purchases, sales, swaps, airdrops, staking rewards, and NFT mints or transfers. You do not need to guess; most major wallets and exchanges provide downloadable CSV files. If you used multiple platforms, export from each one separately. Combine these into a single master spreadsheet before running them through any tax software.

Next, verify your cost basis. The IRS requires you to report the original purchase price or the fair market value at the time of receipt. For NFTs, this is often the ETH or fiat amount paid at minting or acquisition. If you received an NFT as a gift or airdrop, use the fair market value at the time of receipt. Without accurate cost basis data, your gains will be overstated, and your tax bill will be too.

Finally, check for missing forms. If you earned more than $600 in NFT-related income from a marketplace, you should receive a 1099-K. If you did not, you are still liable for the tax. Cross-reference your internal records against any 1099s you receive in January. If they do not match, you must file an amended return or attach a statement explaining the discrepancy. Do not wait for the IRS to notice the gap.

Work through the steps

Filing NFT taxes in 2026 requires more than just summing up sales. The IRS treats digital assets as property, meaning every transaction—minting, trading, gifting, or receiving airdrops—triggers a taxable event. Experts describe the 2026 filing season as a "minefield" for crypto investors due to stricter reporting requirements and complex DeFi interactions [src-serp-2].

Follow this ordered sequence to ensure your NFT tax reporting is accurate and compliant.

Import all your wallet addresses into a crypto tax software. Connect your wallets (like MetaMask) and exchange accounts to pull a complete transaction history. This includes buys, sells, swaps, and any NFTs received as payment or airdrops. Missing even one transaction can lead to IRS discrepancies later.

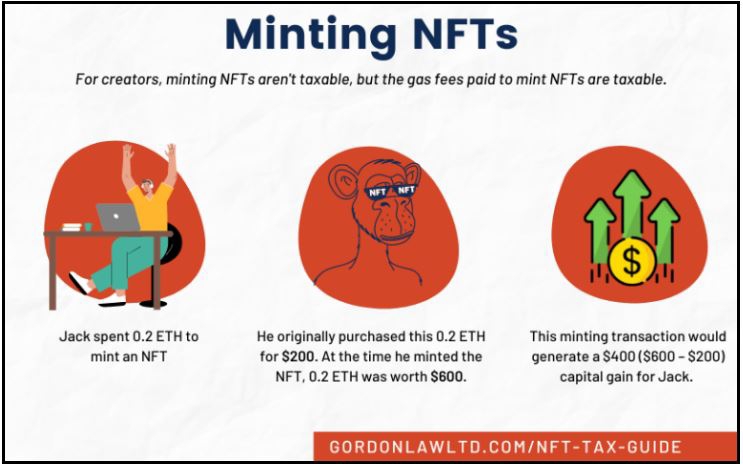

For each NFT you sold or traded, determine the cost basis (what you paid to acquire it) and the fair market value (FMV) at the time of the transaction. If you minted an NFT, your cost basis is typically the gas fees paid. If you received an NFT as income, the FMV at receipt is your income basis.

Not all NFT transactions are capital gains. Categorize them correctly:

- Sale/Trade: Capital gain or loss (Short-term or Long-term depending on holding period).

- Minting: Usually not taxable unless sold immediately.

- Airdrops/Staking Rewards: Taxable as ordinary income at FMV.

- Gifting: Not taxable to the giver, but the recipient inherits the donor’s cost basis.

Subtract your cost basis from the sale price to determine your gain or loss. Use the FIFO (First-In, First-Out) method unless you can specifically identify the NFT sold. Long-term gains (held over one year) are taxed at lower capital gains rates, while short-term gains are taxed as ordinary income.

Enter your NFT transactions on Form 8949, detailing each sale, cost basis, and gain/loss. Summarize the totals on Schedule D. If you received NFTs as income, report that amount on Schedule 1 as ordinary income. Double-check that your software’s generated forms match your manual calculations.

DeFi interactions, such as providing liquidity or using NFTs as collateral, can trigger taxable events. Cross-chain bridges may also be considered sales. Review these complex transactions carefully, as they are often overlooked but carry significant tax implications.

Common Mistakes in NFT Tax Reporting

Filing season for 2026 is shaping up to be a minefield for crypto investors, with many facing messy returns due to avoidable errors. The IRS treats NFTs as property, not just digital collectibles, meaning every transaction triggers a taxable event. When you mix up your basis or ignore specific reporting lines, you risk audits, penalties, or missed deductions.

Here are the three most frequent mistakes that lead to poor outcomes, along with the fixes you need to apply before filing.

1. Confusing Cost Basis with Sale Price

The most common error is reporting the full sale price of an NFT as your taxable gain. This ignores the original purchase price (cost basis), leading to massively inflated tax bills. If you bought an NFT for 0.5 ETH and sold it for 1 ETH, you only owe taxes on the 0.5 ETH profit, not the entire 1 ETH.

The Fix: Always subtract your original acquisition cost from the sale proceeds. If you acquired the NFT through a mint, your basis is the ETH plus gas fees paid at minting. If you received it as a gift, the basis is usually the donor’s original cost, not the fair market value at the time of receipt.

2. Ignoring NFT Staking and Airdrop Income

Many filers only track sales and forget to report income received through staking, airdrops, or rewards. The IRS considers these events as ordinary income at the fair market value of the NFT on the day you received it. Even if you never sell the NFT, you must report this value as income in the year it entered your wallet.

The Fix: Record the USD value of every NFT received as income at the time of receipt. This value then becomes your new cost basis. If you later sell that NFT, your gain or loss is calculated from this new basis, not from zero.

3. Mixing Up Personal and Commercial Use

NFTs used for business purposes, such as marketing assets or commercial licenses, have different tax treatments than personal collectibles. Treating a business NFT as a personal capital asset can lead to incorrect reporting. Conversely, failing to deduct business-related expenses like gas fees or platform commissions reduces your allowable deductions.

The Fix: Clearly separate your NFT portfolio into personal and business categories. For business-use NFTs, track all associated expenses (gas, marketplace fees) as deductible costs. Consult a tax professional to determine if your NFT activities qualify for business expense deductions or if they must be reported as capital gains.

Nft tax 2026: what to check next

The 2026 filing season brings new reporting layers for digital assets. Below are answers to the most common questions about NFT taxes, broker rules, and holding periods.

Filing season will be messy for most crypto investors. Use official sources to verify your cost basis and keep records of every transaction.

No comments yet. Be the first to share your thoughts!