Understand the 2026 reporting changes

The IRS treats non-fungible tokens (NFTs) as property, not currency. This classification means every sale, trade, or exchange triggers a taxable event. You must calculate the difference between your cost basis and the sale price to determine your gain or loss.

Starting in 2026, the reporting landscape shifts significantly. Brokers are now required to report both the gross proceeds and the adjusted cost basis for covered digital assets. These forms will be issued in 2027 for transactions occurring in 2026. This change reduces the ambiguity that previously allowed many traders to underreport their activity.

For NFTs traded on centralized exchanges, the platform will likely provide the necessary data. However, if you trade peer-to-peer or use decentralized marketplaces, you remain responsible for tracking your own records. Accurate tracking is no longer optional; it is mandatory for compliance with the updated Form 1099-DA requirements.

Gather your transaction history

Before the 2026 reporting standards take effect, you need a complete record of every NFT transaction. The IRS is introducing Form 1099-DA, which requires detailed cost basis and sales data. If you rely on manual tracking, you risk missing entries that will later appear on IRS forms, creating discrepancies you must explain.

Start by exporting data from every platform where you traded. Exchanges like Coinbase or Kraken provide CSV downloads of your trade history. Marketplaces such as OpenSea or Blur often allow you to export sales records. For self-custodied wallets, use tools like MetaMask or portfolio trackers to generate a full transaction log. This step is critical because wallet-level tracking becomes harder once new reporting rules apply.

Log into each exchange you used. Go to the "History" or "Transactions" section. Download your trade history in CSV format. Include all buy, sell, and trade records for the tax year.

Go to each NFT marketplace where you listed or purchased items. Look for an "Export" or "Download Data" feature. If unavailable, manually record the date, price, and token ID for each sale. Keep receipts for any platform fees paid.

For non-custodial wallets, use blockchain explorers or portfolio trackers like Etherscan or Zapper. Export your full transaction history. This captures transfers between wallets that exchanges might not report.

-

Exchange trade history (CSV)

-

Marketplace sales and purchase records

-

Wallet transaction exports

-

Platform fee receipts

Keep these records organized in a single folder. You will need them to calculate your gains and losses accurately. The new IRS Form 1099-DA will require precise cost basis data, so having your own records is your best defense against errors.

Calculate your NFT cost basis and gains

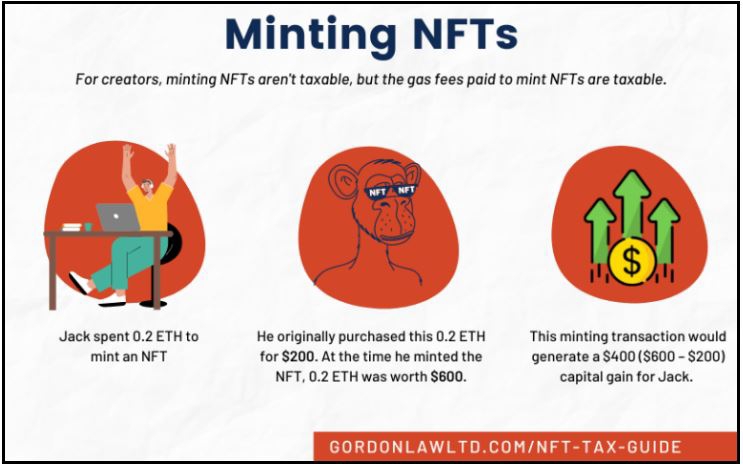

To determine your tax liability, you must subtract the cost basis from the sale price. The cost basis is the total amount you paid to acquire the NFT, including the purchase price and any transaction fees (gas) paid at the time of minting or buying. The sale price is the total amount you received when you sold or traded it, minus any fees paid during the sale.

The formula is straightforward:

Gain/Loss = Sale Price - Cost Basis

For example, if you bought an NFT for 0.1 ETH and paid 0.01 ETH in gas fees, your cost basis is 0.11 ETH. If you later sell it for 0.2 ETH and pay 0.01 ETH in gas, your gross proceeds are 0.19 ETH. Your gain is 0.08 ETH (0.19 - 0.11).

Matching sales to purchases

When you sell an NFT, you must identify which specific purchase it came from. The IRS allows two primary methods for this matching process:

This is the most accurate method. You track each individual NFT by its unique token ID and link it to its specific purchase transaction. This allows you to pick which NFT to sell, potentially minimizing taxes by choosing the one with the highest cost basis or longest holding period. Keep detailed records of each acquisition.

If you cannot identify specific NFTs, the IRS defaults to FIFO. This means the first NFT you acquired is considered the first one sold. This method is simpler but may result in higher taxes if early purchases were made at lower prices.

New cost basis reporting rules

Starting January 1, 2026, new regulations require crypto brokers to report cost basis information alongside gross proceeds. This change aims to improve compliance and simplify reporting for taxpayers. However, these rules primarily apply to centralized exchanges and brokers. Transactions on decentralized exchanges (DEXs) or peer-to-peer trades may still require you to self-report cost basis using your own records.

For more details on how these new rules apply to NFTs, refer to official guidance from the IRS or consult a tax professional specializing in digital assets.

Reconcile Your Records with Form 1099-DA

The 2026 tax season introduces Form 1099-DA, a standardized statement that digital asset brokers must issue for covered transactions. This form reports gross proceeds and adjusted cost basis, shifting the burden of record-keeping from you to the platform. Your first task is to download these forms from every exchange where you traded and compare them against your personal transaction logs.

Reconciliation is not just a formality; it is the primary defense against an IRS notice. Brokers may report transactions incorrectly, especially for complex moves like staking rewards, airdrops, or transfers between wallets. If the numbers on the 1099-DA do not match your internal records, you must investigate the discrepancy before filing.

Start by listing every transaction your personal tracker recorded. Then, pull the corresponding 1099-DA from each broker. Highlight any rows where the cost basis or proceeds differ. Common errors include missing cost basis adjustments for prior-year sales or misclassifying non-taxable events like peer-to-peer transfers.

If you find errors, contact your broker’s support team immediately. Request a corrected 1099-DA if they acknowledge the mistake. If they refuse, keep the correspondence and report the correct amounts on your tax return, noting the discrepancy. The IRS expects you to report the truth, not just what is on a form.

Key Reconciliation Steps

- Download all 1099-DA forms from your brokers for the 2026 tax year.

- Export your transaction history from your personal tax software or spreadsheet.

- Compare gross proceeds and cost basis line by line.

- Flag discrepancies for further investigation or broker correction.

Common Discrepancies

| Issue | Broker Report | Your Records | Action |

|---|---|---|---|

| Missing Cost Basis | $0 | $5,000 | Request correction or adjust on return |

| Non-Taxable Transfer | Taxable Sale | Transfer | Ignore or mark as non-taxable |

| Staking Rewards | Omitted | Included | Add to income on Schedule 1 |

| Airdrop Value | Understated | Market Value | Report fair market value at receipt |

What If the Broker Won’t Correct It?

Brokers are not always right. If a broker refuses to issue a corrected 1099-DA, you are still responsible for reporting the correct tax liability. File your return using your accurate records and attach a statement explaining the discrepancy. Keep all emails and support tickets as proof of your good faith effort. The IRS is more likely to accept your position if you can demonstrate that you tried to resolve the error.

Remember, the 1099-DA is a starting point, not the final word. Your personal records are the source of truth. Treat reconciliation as a critical audit step, not an afterthought.

File your return by the deadline

The easiest mistake with NFT taxes is comparing options on the most visible detail while ignoring the day-to-day constraint. A choice can look strong on paper and still fail because it is too hard to maintain, too expensive to repeat, or awkward in the actual setting.

Use the same checklist for every option: fit, cost, durability, timing, upkeep, and fallback plan. That keeps the comparison practical instead of drifting into preference alone.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Avoid these common NFT tax mistakes

Many creators and investors trigger audits by overlooking specific reporting requirements. The IRS treats NFTs as property, meaning every transaction that changes ownership or value can create a taxable event. Below are the most frequent errors and how to fix them before filing.

Ignoring airdrops and free mints

Receiving an NFT through an airdrop or a free mint is not tax-free. If the NFT has a fair market value when you receive it, that value counts as ordinary income. You must report this amount on your tax return even if you never sold the asset. Failing to track these "free" tokens is a common audit trigger because they often appear on-chain but go unreported.

Misclassifying staking rewards

Staking rewards are generally treated as ordinary income at the moment you receive them, based on the fair market value at that time. Some taxpayers mistakenly classify these as capital gains or ignore them entirely. Correct classification ensures you report the income accurately and establish the correct cost basis for future sales.

Overlooking small transactions

While lawmakers have proposed de minimis exemptions for small crypto payments, no such federal exemption currently exists for NFTs. Transactions under $200 or $300 still count as taxable events if they involve a sale, swap, or disposition. Ignoring small sales because they seem insignificant can lead to underreporting.

Frequently asked questions about NFT taxes

These answers address the specific compliance tasks you need to complete for the 2026 tax year. The rules have shifted significantly from previous years, particularly regarding how cost basis is reported.

For official guidance on the new reporting forms, refer to the IRS instructions for Form 1099-DA.

No comments yet. Be the first to share your thoughts!