What changed for NFT taxes in 2026

The 2026 filing season marks a definitive shift from ambiguous guidance to mandatory compliance for NFT holders. The primary driver of this change is the IRS's new Form 1099-DA, which requires digital asset brokers to report transaction data directly to the agency. This form closes the loophole that previously allowed many off-chain or peer-to-peer NFT transfers to go unreported.

For most crypto investors, experts describe the upcoming filing season as "messy" and a "minefield" due to the volume of new reporting requirements and the complexity of matching these forms to personal transaction histories [Forbes]. If you held, traded, or received NFTs in 2025, you must reconcile your internal records with the data brokers are sending to the IRS.

Failure to file accurately can result in significant penalties. The IRS has signaled that it will treat unreported digital asset income with the same rigor as traditional securities violations. Start by gathering all 1099-DA forms from your exchanges and wallets before attempting to calculate your tax liability.

Gather your transaction history

Before you can calculate your NFT tax liability, you need a complete ledger of every transaction. The standard for accuracy is no longer a single exchange report; it is a wallet-by-wallet accounting of your entire digital footprint.

Start by exporting CSV files from every centralized exchange where you traded. Platforms like Coinbase, Binance, and Kraken provide transaction histories, but these reports often miss off-exchange activity or internal transfers. Treat these exports as the baseline, not the final word. If you held NFTs in a self-custody wallet, these exchange reports will be incomplete.

Next, pull data directly from blockchain explorers for your self-custody wallets. Tools like Etherscan or Solscan allow you to view transaction histories for specific wallet addresses. This step is essential for capturing peer-to-peer sales, minting events, and airdrops that never touched a centralized platform. Export these records as CSVs to keep your data consistent.

Finally, aggregate all your CSVs into a single tax software tool. Manual reconciliation is prone to error, especially when dealing with hundreds of transactions across multiple chains. Dedicated NFT tax software can import these files, identify wash sales, and calculate your cost basis automatically. This aggregation step turns raw data into a format the IRS expects.

Log into each centralized exchange you used. Navigate to the tax or reports section and download the full transaction history for the tax year. Ensure you include all trading pairs involving NFTs or NFT-related tokens.

Identify every self-custody wallet address you used. Use blockchain explorers to view and export transaction histories for each address. This captures direct sales, minting, and transfers that exchanges do not report.

Import all CSV files into a reputable NFT tax software tool. The software will reconcile transactions, identify duplicates, and calculate your capital gains or losses. This creates a single, audit-ready report.

Classify sales, mints, and royalties

Tax rules for NFTs depend on your role. Collectors generally pay capital gains tax when they sell or trade. Creators pay ordinary income tax on royalties and initial sales. The IRS treats these as distinct events with different rates and reporting requirements.

Collector tax treatment

When you sell an NFT, the tax depends on how long you held it. If you held the NFT for less than a year, the profit is taxed as short-term capital gains. These are taxed at your ordinary income tax rate, which ranges from 10% to 37% in 2026 [src-serp-4].

If you held the NFT for more than a year, you qualify for long-term capital gains rates. These rates are typically lower, capped at 15% or 20% depending on your income [src-serp-3]. Trading NFTs for other crypto assets is a taxable event, not a gift. You must calculate the fair market value at the time of the trade.

Creator tax treatment

Creators face a different tax structure. Income from primary sales and secondary royalties is treated as ordinary income. This means it is taxed at your marginal income tax rate, which can be up to 37% [src-serp-7].

Royalties are also subject to self-employment tax if you are considered a self-employed artist. This adds an additional 15.3% on top of income tax. You must report this income on Schedule C. Keep detailed records of minting costs and gas fees to offset your taxable income.

Comparison of tax rates

The table below summarizes the key differences between collector and creator tax obligations.

| Role | Taxable Event | Tax Rate | Notes |

|---|---|---|---|

| Collector | Sale (<1 year) | 10-37% | Short-term capital gains |

| Collector | Sale (>1 year) | 0-20% | Long-term capital gains |

| Creator | Primary Sale | Up to 37% | Ordinary income |

| Creator | Royalties | Up to 37% + 15.3% | Ordinary income + self-employment tax |

Calculate gains and losses correctly

Determining the correct cost basis for an NFT requires tracking two distinct transactions: the purchase of the digital asset and its eventual disposal. Because NFTs are typically bought with cryptocurrency, the initial acquisition is itself a taxable event. You must calculate the fair market value of the crypto used to pay for the NFT at the exact moment of exchange. This value becomes your cost basis. If the cryptocurrency has appreciated since you acquired it, you owe taxes on that gain immediately, separate from any NFT-specific gains or losses.

When you eventually sell, trade, or otherwise dispose of the NFT, you compare the proceeds against this established cost basis. The difference determines your capital gain or loss. It is critical to distinguish between short-term and long-term holding periods, as the tax rate applied depends entirely on how long you held the asset. The Internal Revenue Service treats these holdings differently, so accurate date tracking is essential to avoid overpaying or facing penalties.

Determine the initial cost basis

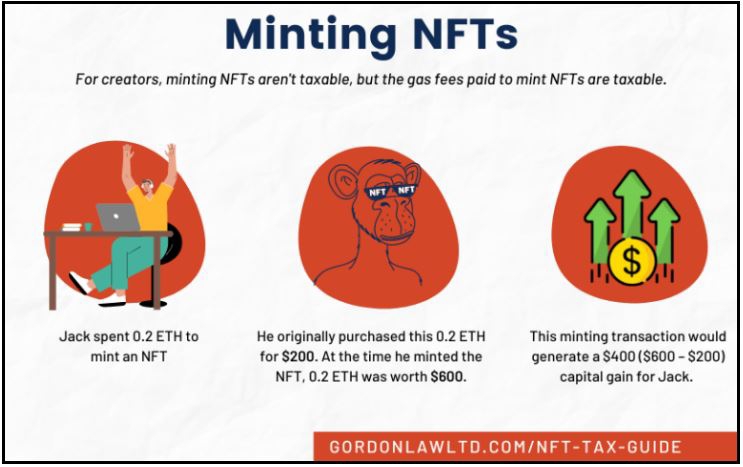

Your cost basis is not just the amount of crypto sent; it is the dollar value of that crypto at the time of the transaction. For example, if you bought an NFT using 0.5 ETH, and 0.5 ETH was worth $1,500 on that date, your cost basis is $1,500. This figure also includes any gas fees paid to complete the transaction, as these are considered part of the acquisition cost. Keep records of the exact timestamp and the exchange rate at that moment.

Apply the correct holding period

The IRS classifies NFT holdings as either short-term or long-term based on the duration you held the asset before disposal. If you held the NFT for one year or less, it is a short-term holding. Gains are taxed at your ordinary income tax rate, which can range from 10% to 37% depending on your bracket. If you held it for more than one year, it qualifies for long-term capital gains rates, which are generally lower and tiered at 0%, 15%, or 20%. Misclassifying the holding period is a common source of errors.

Calculate the final gain or loss

Subtract your total cost basis (crypto value + gas fees) from the amount you received when you sold or traded the NFT. If the result is positive, you have a taxable gain. If negative, you have a capital loss that may offset other gains. Ensure you use the same valuation method for both the purchase and sale to maintain consistency. For official guidance on capital asset taxation, refer to IRS Publication 544.

Common mistakes that trigger audits

Digital asset tax experts warn that the process will be particularly messy for those who misunderstand how NFTs interact with existing tax codes [src-serp-2]. Most audits stem from simple oversights rather than complex evasion. You can avoid these pitfalls by treating every NFT interaction as a taxable event, regardless of how it entered your wallet.

Ignoring fiat purchases of NFTs

Many collectors believe that buying an NFT with fiat currency is a tax-free entry point. This is incorrect. If you purchase an NFT using cryptocurrency, that swap is a taxable disposition of the crypto. You must report the capital gain or loss on the crypto you spent at the time of the transaction [src-serp-6]. Failing to track the cost basis of the crypto used to buy the NFT creates a gap in your records that the IRS can easily flag.

Failing to report airdrops as income

Receiving an NFT via an airdrop is not free money; it is taxable income. The fair market value of the NFT at the moment you gain control of it must be reported as ordinary income on your tax return. Even if the NFT has no immediate liquidity or market value, the IRS generally expects you to report the value at the time of receipt. Ignoring airdrops is a common trigger for audits because blockchain data is public and immutable.

Assuming wash sale rules apply

A frequent misconception is that the wash sale rule—which prevents investors from claiming a loss if they buy a "substantially identical" asset within 30 days—applies to cryptocurrencies and NFTs. For individual taxpayers in 2026, this rule generally does not apply to digital assets. However, relying on this exception requires careful documentation. If you sell an NFT at a loss and buy it back shortly after, you can claim that loss, but you must prove the transactions clearly. Do not assume the IRS will automatically apply these rules in your favor without precise records.

Finalize your return with a checklist

Before you submit, ensure every transaction is accounted for. The IRS asks a single yes/no question about crypto activity on the main return, but the details belong in the supporting schedules. Missing a wallet or miscalculating cost basis can trigger audits or penalties, so treat this step with the same rigor as your W-2 filing.

Pre-Filing Verification

- Include all wallets: Verify that every address used during the tax year is listed, including cold storage and exchange accounts.

- Confirm cost basis: Double-check that your initial purchase price and fees are accurate for every NFT sold or swapped.

- Check for 1099-DA forms: Ensure any new IRS reporting forms received from exchanges are attached or reconciled.

- Review for common errors: Look for duplicate entries or missed airdrops that might have been overlooked during aggregation.

Once these items are verified, you are ready to file your NFT taxes with confidence.

No comments yet. Be the first to share your thoughts!