2026 broker reporting rules

For the 2026 tax season, the IRS shifts the burden of proof from the taxpayer to the exchange. Under the new digital asset broker rules, platforms must now report cost basis and gain/loss data for transactions occurring on or after January 1, 2026. This change applies to digital assets acquired from and held with the broker, fundamentally altering how NFTs and metaverse collectibles are reported.

Previously, taxpayers had to manually track the acquisition cost of every NFT sale. Now, centralized exchanges and certain decentralized platforms acting as brokers will file Form 1099-B with the IRS. This data includes the original purchase price, the sale proceeds, and the resulting capital gain or loss. The IRS receives this information directly, meaning discrepancies between your tax return and the broker’s report will be flagged automatically.

This shift is critical for NFT collectors who traded on major platforms. If you bought an AI collectible in 2025 and sold it in 2026, the exchange must report the basis. For transactions before 2026, you remain responsible for calculating and reporting the cost basis yourself. Keep your original transaction records, as they may still be needed to reconcile older holdings or if the broker’s data is incomplete.

The rules are detailed in the IRS guidance on digital asset reporting. Ensure your exchanges are compliant and that your account information is up to date to avoid delays in receiving your tax forms. IRS Notice 2023-66 outlines the specific requirements for digital asset brokers.

Categorize your NFT transactions correctly

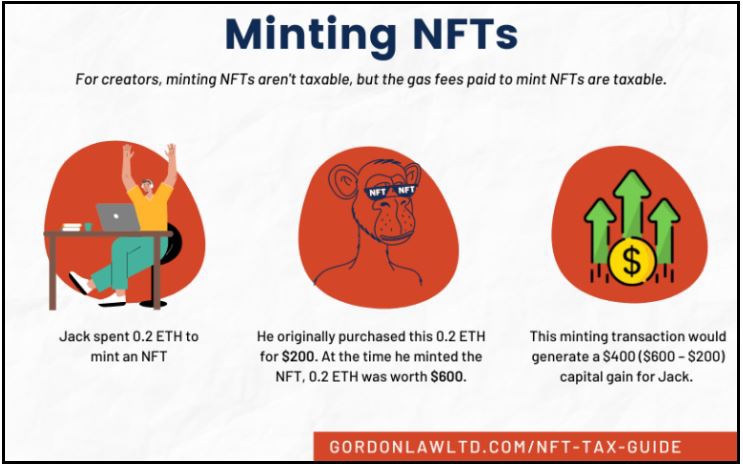

How you classify an NFT transaction determines your tax rate. The IRS treats digital assets as property, but the source of the transaction changes the category. Selling an NFT you already own is a capital gain. Minting, staking, or receiving an airdrop is ordinary income. Misclassifying these events can lead to underpayment penalties or audits.

The difference matters significantly. Capital gains rates are generally lower than ordinary income rates. However, short-term capital gains are taxed at your regular income bracket. Long-term gains apply only if you held the asset for more than one year. Creators often face higher rates because royalties and minting proceeds are treated as self-employment income.

Use the table below to identify how your specific NFT activity is taxed. This classification is the first step in accurate reporting.

| Activity | Tax Category | Typical Rate |

|---|---|---|

| Selling owned NFT | Capital Gain | 0%, 15%, or 20% (Long-term) |

| Trading NFT for ETH | Capital Gain | 0%, 15%, or 20% (Long-term) |

| Minting an NFT | Ordinary Income | Up to 37% + Self-Employment Tax |

| Staking Rewards | Ordinary Income | Up to 37% |

| Airdrops | Ordinary Income | Up to 37% |

Track wallet activity and cost basis

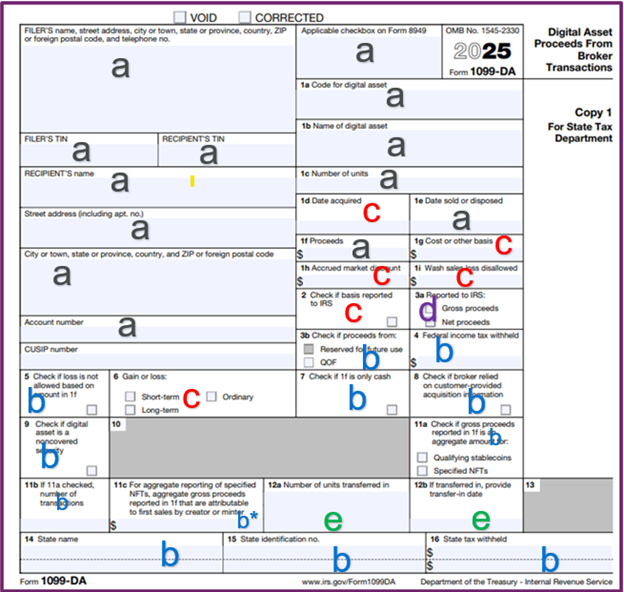

The 2026 filing season introduces Form 1099-DA, requiring precise reporting of digital asset transactions. To comply, you must gather transaction history from every wallet and exchange used during the tax year. This process establishes your cost basis and determines your capital gains or losses.

1. Export data from centralized exchanges

Log into each exchange where you traded NFTs or crypto. Go to the transaction history or tax reporting section. Download the full CSV or JSON export for the entire tax year. Ensure the data includes dates, asset types, amounts, and fair market values at the time of each transaction.

Locate the tax or compliance section in your exchange dashboard. Select the relevant tax year and export all transaction records. Verify that the file includes all trades, sales, and transfers.

Review the downloaded file for gaps. Cross-reference with your email confirmations or account statements. Missing records can lead to underreporting or IRS audits.

2. Aggregate on-chain wallet data

Centralized exchanges do not report activity from self-custody wallets. Use a blockchain explorer or tax software to import your wallet addresses. This captures transactions that occurred directly on the blockchain, such as peer-to-peer NFT sales or swaps on decentralized exchanges.

Connect your wallet addresses to your tax preparation tool. The software will scan the blockchain for all incoming and outgoing transactions associated with those addresses.

Merge the on-chain data with your exchange exports. Identify duplicate transactions that may have been reported by both the exchange and the blockchain scanner. Remove duplicates to avoid double taxation.

3. Calculate cost basis for each NFT

For each NFT you sold, determine the original purchase price. This is your cost basis. If you received the NFT as a gift or reward, the basis may be different. Accurate cost basis calculation is essential for determining your taxable gain or loss.

For each NFT sold, record the price paid when you acquired it. If you acquired it through a mint, use the minting fee. If you bought it on a marketplace, use the purchase price.

Note the date you acquired each NFT and the date you sold it. This determines whether your gain is short-term or long-term, which affects your tax rate.

4. Prepare for Form 1099-DA reporting

With all data aggregated and reconciled, you are ready to report your activity on Form 1099-DA. Ensure all transactions are categorized correctly as sales, exchanges, or other dispositions. Keep your records for at least three years in case of an audit.

Review your final transaction list. Mark each item as a sale, exchange, or other disposition. Ensure all fields are complete and accurate before filing.

Save all export files, wallet addresses, and transaction confirmations. These documents serve as proof of your cost basis and holding periods if the IRS requests verification.

5. Review and file

Before submitting your tax return, review your calculations one last time. Check for any missed transactions or incorrect cost basis entries. If you are unsure about any aspect of your reporting, consult a tax professional specializing in digital assets.

AI-Generated Collectibles: Ownership and Tax Timing

AI-generated NFTs introduce a distinct layer of complexity because the "creation" event is no longer a single moment of artistic effort, but a series of automated outputs. The IRS treats the minting of an AI-generated asset as a taxable event if it is created for sale or exchange. You must recognize that the act of generating the image or audio file does not create intellectual property rights in the same way traditional authorship does, which complicates how you report the initial value.

Determine Ownership Rights

Before calculating taxes, you must establish whether you hold the copyright to the AI output. In most jurisdictions, purely AI-generated works are not eligible for copyright protection because they lack human authorship. This means you cannot claim ownership in the traditional sense, but you still hold the token as property. If you are minting AI art to sell, the IRS views the proceeds as ordinary income, not capital gains, at the point of sale. The lack of copyright does not exempt you from reporting the transaction; it simply limits your ability to enforce ownership against infringers.

Report Creation as Income

When you mint an AI-generated collectible, you are essentially creating an asset with a fair market value. If you intend to sell it, the IRS requires you to report the fair market value of the token at the time of minting as ordinary income. This is often the most confusing part for creators: you pay tax on income you haven't yet realized in cash. For example, if your AI tool generates a piece you mint and list for 1 ETH, you report 1 ETH as income, even if you never sell it. If you later sell it, the difference between that initial value and the sale price is a capital gain or loss.

Track Basis Carefully

Your cost basis for an AI-generated NFT is typically the fair market value at the time of minting. If you created the AI file yourself using free or subscription-based tools, your basis is the market value of the token when it hits the blockchain, not the cost of your software subscription. Keep detailed records of the minting date, the ETH price at that moment, and the transaction hash. If you hold the NFT for more than a year before selling, the profit above your basis is taxed at long-term capital gains rates. If you sell quickly, it is short-term. Misreporting the basis as zero or the software cost will trigger audits.

File your return using the correct forms

Filing your 2026 tax return with digital assets requires precision. The IRS treats NFTs, metaverse land, and AI collectibles as property, not currency. This classification triggers specific reporting requirements that differ from standard investment filings. Missing a single line item can result in audits or penalties, especially as the 2026 filing season is already described by experts as a "minefield" for crypto investors [src-serp-2].

Your filing journey begins with the digital asset question on Form 1040. This is your primary compliance trigger. If you received, sold, exchanged, or gifted any NFTs during the tax year, you must answer "yes" to this question. This simple binary choice signals to the IRS that you have additional schedules to complete. Do not ignore this question; a false "no" when you have transacted is considered tax fraud.

Next, you must report each transaction on Form 8949, Sales and Other Dispositions of Capital Assets. Unlike traditional stocks, NFT transactions often lack third-party 1099-B forms from exchanges. You are responsible for calculating the gain or loss for every individual sale, swap, or mint. List each transaction separately on Form 8949, including the date acquired, date sold, proceeds, and cost basis.

Finally, transfer the totals from Form 8949 to Schedule D, Capital Gains and Losses. Schedule D summarizes your total capital gains and losses, which then flow to your main Form 1040. Keep detailed records of every transaction, including timestamps and wallet addresses, to substantiate your cost basis if the IRS requests proof.

Common questions about NFT taxes

Tax authorities have tightened enforcement around digital assets. Below are specific answers to frequent compliance questions for 2026.

No comments yet. Be the first to share your thoughts!